The American economic system has an unimaginable historical past of manufacturing probably the most helpful corporations on the planet. Metal in america grew to become the first-ever billion-dollar firm in 1901, and 117 years later in 2018, Apple grew to become the primary firm on the planet to succeed in a valuation of $1 trillion.

Apple is now value greater than $3.7 trillion, and 6 different tech corporations have joined it within the trillion-dollar membership: Microsoft, Amazon, Alphabet, Metaplatforms, TeslaAnd Nvidia. However I believe one other one would possibly quickly acquire traction.

Oracle(NYSE:ORCL) was based in 1977 and has participated in virtually each technological revolution since then. Right now, the corporate is rapidly changing into a frontrunner in synthetic intelligence (AI) information heart infrastructure, which may propel the corporate to a valuation of lower than $1 trillion of a decade.

Oracle’s market capitalization at the moment stands at $492 billion. Buyers who purchase its shares at the moment may due to this fact double their stake in the event that they joined the trillion-dollar membership.

Large language models (LLM) are the muse of each chatbot and AI software program software. Builders proceed to create bigger LLMs to make AI software program “smarter,” however it is a very costly train that requires information facilities stuffed with 1000’s of graphics processing models (GPUs) .

Nvidia gives the world’s strongest GPUs for growing AI. The extra a developer can entry, the extra information their LLMs can ingest and course of. Oracle Cloud Infrastructure (OCI) Supercluster expertise permits builders to scale as much as 65,000 Nvidia H200 GPUs, which is the very best quantity within the business.

However Oracle is about to go additional. It’s at the moment constructing new clusters that may permit builders to make use of as much as 131,000 of Nvidia’s latest Blackwell GPUs.

OCI’s Direct Reminiscence Entry (RDMA) expertise can be a lot sooner than conventional Ethernet networks on the subject of shifting information from one level to a different. Since most builders lease compute capability on a per-minute foundation, sooner processing interprets into substantial financial savings. For this reason Oracle has attracted main AI startups akin to xAI, OpenAI, Cohere, and so forth.

Throughout its second quarter of fiscal 2025 (which ended October 31), Oracle stated GPU utilization elevated 336% from the year-ago interval, placing spotlight how rapidly demand for AI infrastructure is rising. The corporate at the moment has 98 information facilities in operation, but it surely plans to construct 1,000 to 2,000 extra in the long run to satisfy this demand.

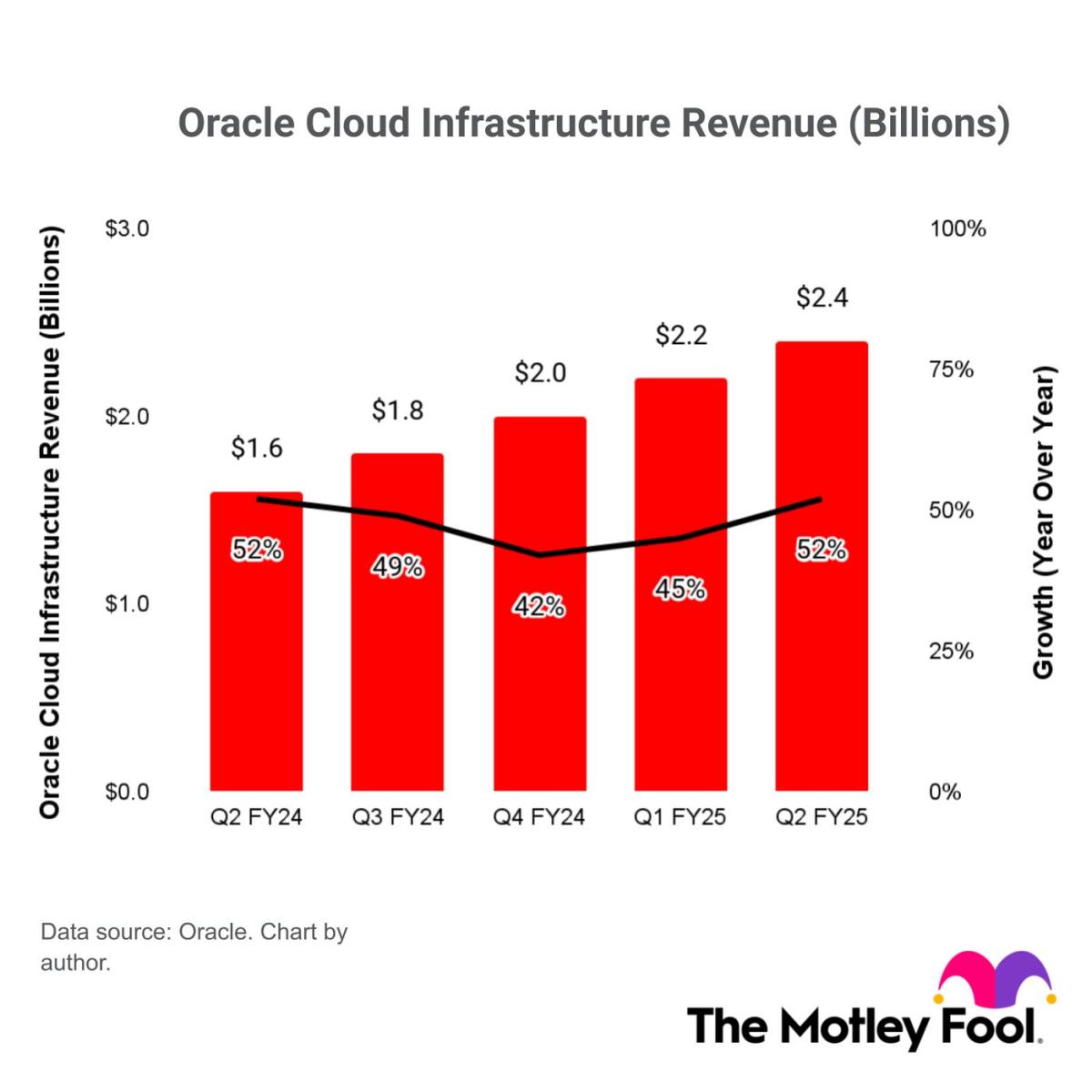

Oracle generated whole income of $14.1 billion through the second quarter, a rise of 9% from final 12 months. However OCI income, particularly, soared 52% to a report $2.4 billion. That is the quickest progress fee in a 12 months, and is the second consecutive quarter of acceleration after a quick decline:

A chart of Oracle Cloud Infrastructure’s quarterly income and progress fee.

Merely put, OCI’s income would develop even sooner if extra information facilities have been operational. Although the corporate builds them as rapidly as potential, it nonetheless struggles to maintain up with demand.

That is a part of the explanation why Oracle’s remaining efficiency obligations (RPOs) jumped 50% 12 months over 12 months to $97 billion within the second quarter. RPOs are like an order ebook that’s anticipated to show into income sooner or later as soon as Oracle is ready to present the agreed upon companies. CEO Safra Catz stated RPOs will improve even farther from right here, citing a current deal Oracle signed with Meta Platforms.

Meta developed the world’s hottest open supply LLMs, known as Llama, which have been downloaded over 600 million instances. The corporate will transfer a few of its coaching workloads to Oracle’s infrastructure, and the 2 corporations will collaborate to create AI brokers utilizing Llama. This can be a large win for Oracle provided that Llama 4 may very well be probably the most superior mannequin within the business when it launches subsequent 12 months (in response to Meta CEO Mark Zuckerberg).

Oracle generated $4.09 in earnings per share (EPS) over the past 4 quarters. So, primarily based on its inventory worth of $177.74 on the time of writing, it’s buying and selling at a price-to-earnings (P/E) ratio of 43.4. It is not precisely low cost contemplating the Nasdaq-100 the tech index trades at a P/E ratio of simply 33.9.

Nonetheless, Oracle grew its EPS by 24% through the second quarter, which was the quickest tempo in virtually a 12 months. The corporate’s information facilities are extremely automated, so they’re extremely low cost to function and due to this fact generate excessive revenue margins. As extra of them come on-line, the economies of scale ought to translate into very robust revenue progress for Oracle.

Mathematically talking, Oracle’s market cap may exceed $1 trillion inside 10 years if the corporate grows its EPS by 7.3% per 12 months (assuming its present price-to-earnings ratio stays fixed). Contemplating the corporate plans to broaden its information heart footprint tenfold From right here, I believe its EPS progress is extra prone to speed up reasonably than decelerate over the approaching decade.

Due to this fact, 10 years is a very a prudent timeframe for Oracle to affix the $1 trillion membership. It may obtain this in lower than 4 years if it maintains EPS progress of no less than 20%.

Have you ever ever felt such as you missed the boat by shopping for the very best performing shares? Then you’ll want to hear this.

On uncommon events, our group of professional analysts points a “Doubled” actions advice for companies that they imagine are on the snapping point. Should you’re anxious that you’ve got already missed your probability to take a position, now could be the very best time to purchase earlier than it is too late. And the numbers converse for themselves:

Nvidia:Should you invested $1,000 after we doubled down in 2009,you’ll have $356,125!*

Apple: Should you invested $1,000 after we doubled down in 2008, you’ll have $46,959!*

Netflix: Should you invested $1,000 after we doubled down in 2004, you’ll have $499,141!*

Proper now, we’re issuing “Double Down” alerts for 3 unimaginable corporations, and there will not be one other probability like this anytime quickly.

John Mackey, former CEO of Complete Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Suzanne Frey, an government at Alphabet, is a member of The Motley Idiot’s board of administrators. Randi Zuckerberg, former director of market improvement and spokesperson for Fb and sister of Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Idiot’s board of administrators. Anthony DiPizio has no place in any of the shares talked about. The Motley Idiot holds positions and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, Oracle and Tesla. The Motley Idiot recommends the next choices: lengthy January 2026 $395 calls on Microsoft and quick January 2026 $405 calls on Microsoft. The Motley Idiot has a disclosure policy.