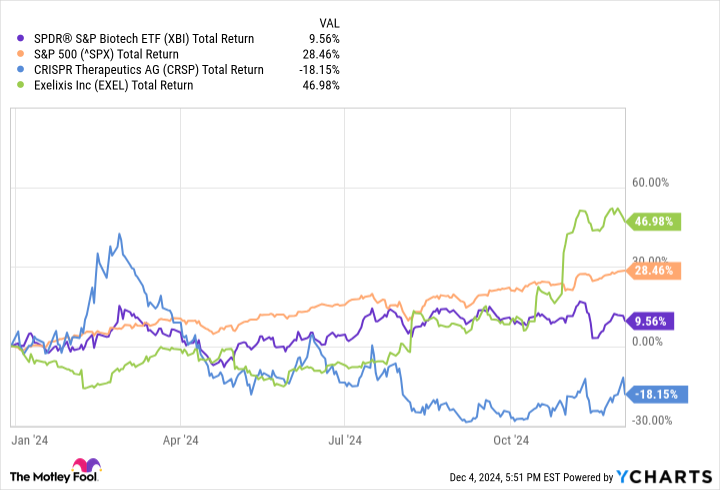

The biotech business is lagging behind the broader market up to now in 2024. SPDR S&P Biotechnology ETFsector benchmark, is up 9% this 12 months in comparison with 28% for the S&P500. Will this development proceed in 2025? It's exhausting to say, however many particular person biotech shares nonetheless seem like strong long-term picks.

This consists of CRISPR therapeutics(NASDAQ:CRSP) And Exelixis(NASDAQ:EXEL). The previous is effectively within the pink for the 12 months, whereas the latter has crushed the complete market this 12 months. Though transferring in reverse instructions in 2024, CRISPR Therapeutics and Exelixis have sturdy prospects. Learn on to search out out extra.

Lacking the morning scoop?Breakfast Information delivers it multi function quick, silly, free day by day publication. Register for free »

CRISPR Therapeutics is a gene-editing specialist with main fame: it created Casgevy, the primary accredited drug that makes use of the Nobel Prize-winning CRISPR approach. The corporate developed this remedy with the assistance of Vertex Prescribed drugs.

Casgevy's first approval was obtained in November 2023, however CRISPR Therapeutics shares have since underperformed the market. What offers? First, Casgevy has but to contribute a single greenback to the biotech's gross sales because of the complexity of administering gene-editing therapies. Second, CRISPR Therapeutics stays unprofitable.

This isn’t uncommon for a biotechnology company of this measurement, however traders have been much less forgiving of unprofitable corporations in recent times. Regardless of these points, CRISPR Therapeutics seems to be a sexy inventory.

Think about Casgevy's potential. The drug treats two uncommon blood issues: transfusion-dependent beta thalassemia (TDT) and sickle cell illness (SCD). There are few therapy choices for both. CRISPR Therapeutics has little competitors in america and nearly none in different areas equivalent to Europe, Saudi Arabia and Bahrain. Their goal market is roughly 58,000 sufferers.

Assuming they will deal with 20,000 sufferers for a median worth of $1.5 million, this might symbolize a $30 billion alternative. Casgevy will price $2.2 million within the US, however we don't know its worth in different international locations. Both manner, the drug has huge potential earlier than even contemplating potential label extensions. And this may very well be just the start for CRISPR Therapeutics.

Regardless of its gradual progress, biotech Casgevy doesn’t lack funds, due to its partnership with Vertex Prescribed drugs. CRISPR Therapeutics ended the third quarter with $1.9 billion in money and equivalents and a number of other thrilling Section 1 and Section 2 gene modifying candidates.

It received't occur in a single day, however between Casgevy's contributions, innovation capabilities, and CRISPR Therapeutics' thrilling pipeline, which can virtually actually ship scientific victories within the years to come back, the corporate can bounce again after his horrible efficiency this 12 months. For this reason CRISPR Therapeutics is value investing in now.

There may be one main purpose for Exelixis' sturdy efficiency this 12 months. The corporate secured a major regulatory victory that may maintain generic competitors for its most cancers drug Cabometyx off the market till 2030.

Cabometyx, which treats sure liver and kidney illnesses, is Exelixis' most essential product. The therapy has confirmed to be a pipeline right into a drug, continually creating new indications whereas remaining essentially the most prescribed therapy of its variety in a few of its markets.

It appears to be like like this formulation will proceed to work. Exelixis is awaiting additional label expansions for its crown jewel, together with the therapy of pancreatic neuroendocrine tumors (pNET). Cabometyx carried out so effectively in a section 3 examine in pNET sufferers that, after an interim evaluation, an unbiased monitoring committee advisable untimely termination of the trial. It appears very possible that the drug will profit from a brand new key label growth.

On the identical time, Exelixis' monetary outcomes stay sturdy. The corporate's third-quarter income elevated 14% 12 months over 12 months to $539.5 million. Exelixis' adjusted earnings per share of $0.47 was effectively above the $0.10 reported a 12 months in the past.

Cabometyx is anticipated to proceed producing regular income progress for a while. As well as, Exelixis is creating different most cancers medicine. It’s conducting a number of section 3 research on zanzalintinib, a product it hopes to observe within the footsteps of Cabometyx. Exelixis additionally gives a number of startup applications.

The corporate's shares might have soared this 12 months, however there may be nonetheless loads of upside potential for traders in it right now who sit tight and maintain the shares for some time.

Have you ever ever felt such as you missed the boat by shopping for the perfect performing shares? Then you’ll want to hear this.

On uncommon events, our staff of knowledgeable analysts points a “Doubled” actions suggestion for companies that they consider are on the breaking point. Should you're apprehensive that you simply've already missed your probability to take a position, now’s the perfect time to purchase earlier than it's too late. And the numbers converse for themselves:

Nvidia:Should you invested $1,000 after we doubled down in 2009,you’d have $369,349!*

Apple: Should you invested $1,000 after we doubled down in 2008, you’d have $45,990!*

Netflix: Should you invested $1,000 after we doubled down in 2004, you’d have $504,097!*

Proper now, we're issuing “Double Down” alerts for 3 unbelievable corporations, and there might not be one other probability like this anytime quickly.

Prosper Junior Bakiny holds positions in Exelixis and Vertex Prescribed drugs. The Motley Idiot ranks and recommends CRISPR Therapeutics, Exelixis and Vertex Prescribed drugs. The Mad Motley has a disclosure policy.