One in all my favourite methods so as to add cash to my portfolio is to spend money on compound corporations which have a confirmed monitor report of outperforming the market after short-term downturns. This concept is very true when the shares in query are buying and selling at what may show to be once-in-a-decade alternatives.

Two corporations that now match this description are animal well being specialists. Idexx Laboratories(NASDAQ:IDXX) And Zoétis(NYSE:ZTS). Whereas Idexx is already one in every of my daughter’s high holdings and Zoetis is one in every of mine, I strongly agree that including your long-term winners over time is a outperforming proposition – a notion espoused by Motley Idiot co-founder David Gardner.

Idexx and Zoetis are at the moment down 37% and 28%, respectively, from their all-time highs, however they’re nonetheless beating the S&P500 on a total return foundation over the previous decade. Here is why buyers ought to take into account proudly owning these two magnificent S&P 500 shares as 2025 approaches.

The Bureau of Financial Evaluation estimates that People spent a complete of $186 billion on their pets in 2023. This determine has almost doubled since 2014, highlighting the megatrend of “pet humanization” that’s anticipated to propel each shares to new heights.

Idexx Labs ought to profit from this due to its leading position in pet health care diagnostics. With an put in base of greater than 144,000 devices worldwide – a determine that grew 10% year-over-year in its most up-to-date quarter – Idexx’s choices detect a variety of illnesses that our four-legged buddies are confronted.

What makes this a high inventory to contemplate is that the corporate has constructed a strong razor and blade mannequin. Its giant base of put in devices constitutes the “razor”. This permits it to generate recurring purchases of merchandise equivalent to check cartridges, reference laboratory recommendation (i.e. assist in decoding check outcomes), consulting companies and subscriptions. to software program. These “blade” gross sales symbolize 80% of Idexx’s turnover.

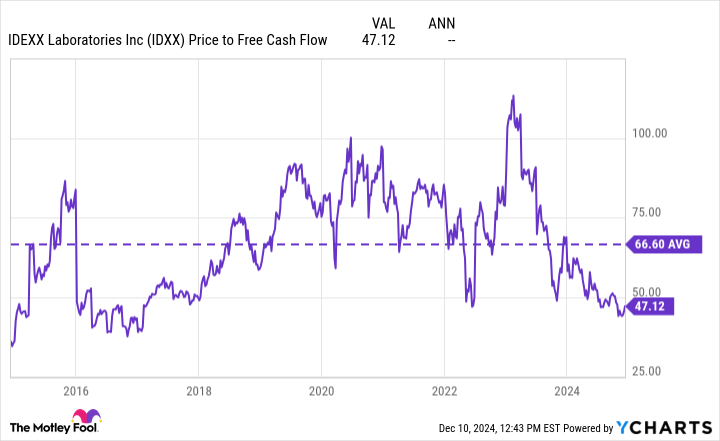

Because of the soundness inherent on this mannequin, Idexx shares have loved a excessive valuation, buying and selling on common at 67 instances free money movement (FCF) over the previous decade.

Nonetheless, as its gross sales progress has fallen from greater than 20% on the top of the pandemic-propelled pet adoption growth to lower than 7% at the moment, the value/FCF valuation of the The corporate fell under 47, a degree it hasn’t seen since. 2016.

I believe this way more cheap valuation helps make the inventory a once-in-a-decade funding alternative as Idexx seems into its new progress market: oncology. It plans to develop its panel of most cancers screening assessments over the subsequent three years to detect roughly 50% of canine most cancers instances.

As pet house owners routinely go for early detection of most cancers slightly than settling for remedy after the very fact, its growth into this $2.5 billion market seems to be a win-win for everybody concerned.

And do not take my phrase for it: Idexx inventory seems promising. Administration lately introduced that it was including a further 5 million shares to its inventory repurchase authorization, which beforehand had 1.3 million shares remaining. The corporate has roughly 82 million shares excellent, so this buyback may assist considerably enhance the inventory value, down 37% from its peak.

Whereas Idexx is the chief in animal well being diagnostics, Zoetis is the chief in drugs, vaccines, genetic testing and precision well being merchandise for pets and livestock. The animal well being big generates 90% of its turnover in classes the place it considers itself a frontrunner in market share.

What makes it such a promising funding is that its dominance comes not simply from one or two medication, however slightly from 15 distinct “blockbusters” that every generate greater than $100 million a 12 months.

Nonetheless, for a similar causes that utilized to Idexx, Zoetis noticed its gross sales progress climb to over 20% in 2021, then drop to a minimal enhance in 2022. This flattening of its progress trajectory prompted the market to considerably scale back the valuation of Zoetis. . At the moment, it trades at 35 instances FCF, nicely under its 10-year common.

Zoetis is now at its lowest value/FCF valuation since 2019 and with its dividend yield again at nearly 1% – slightly below its all-time excessive – Zoetis additionally seems like a once-in-a-decade alternative.

And its dividend appears solely sustainable. As the corporate solely makes use of 33% of its FCF to fund its distributions, Zoetis ought to simply be capable to elevate its dividend for the twelfth 12 months in a row – and past.

Better of all, for buyers, the corporate is having large success within the osteoarthritis market with its new painkillers Librela for canines and Solensia for cats. Mixed gross sales of those two medication elevated 97% throughout the firm’s most up-to-date quarter and have grow to be common choices for pet house owners trying to relieve ache for his or her furry companions.

With the common life expectancy of canines and cats rising by 1.3 and 1.9 years respectively since 2010, osteoarthritis will solely grow to be a extra widespread illness in pets, increasing the marketplace for these drugs .

Down 28% from its 2022 all-time excessive, Zoetis pairs completely with Idexx to kind a duo of S&P 500 animal well being shares poised to outperform the marketplace for years to return .

Have you ever ever felt such as you missed the boat by shopping for the most effective performing shares? Then it would be best to hear this.

On uncommon events, our group of skilled analysts points a “Doubled” actions advice for companies that they imagine are on the breaking point. For those who’re fearful that you have already missed your probability to speculate, now could be the most effective time to purchase earlier than it is too late. And the numbers communicate for themselves:

Nvidia:For those who invested $1,000 after we doubled down in 2009,you’d have $356,125!*

Apple: For those who invested $1,000 after we doubled down in 2008, you’d have $46,959!*

Netflix: For those who invested $1,000 after we doubled down in 2004, you’d have $499,141!*

Proper now, we’re issuing “Double Down” alerts for 3 unbelievable corporations, and there might not be one other probability like this anytime quickly.

Josh Kohn Lindquist holds positions in Idexx and Zoetis Laboratories. The Motley Idiot posts and recommends Zoetis. The Motley Idiot recommends Idexx Laboratories. The Motley Idiot has a disclosure policy.