CRISPR therapeutics(NASDAQ:CRSP) is acknowledged as a pioneer within the area of gene remedy. This biotechnology has the potential to revolutionize medication by way of exact modifications of an individual’s DNA to deal with and treatment genetic ailments. In 2023, the corporate’s sickle cell product Casgevy turned the first-ever CRISPR-based remedy accredited by the Meals and Drug Administration (FDA), marking a major milestone for the corporate.

Nonetheless, commercialization has been gradual, with the market already ready for the following blockbuster drug. As of writing, CRISPR Therapeutics shares are down 46% from their 52-week excessive, main buyers to surprise what’s subsequent. For those who’re contemplating shopping for shares of this gene remedy pioneer, listed below are three issues you could know.

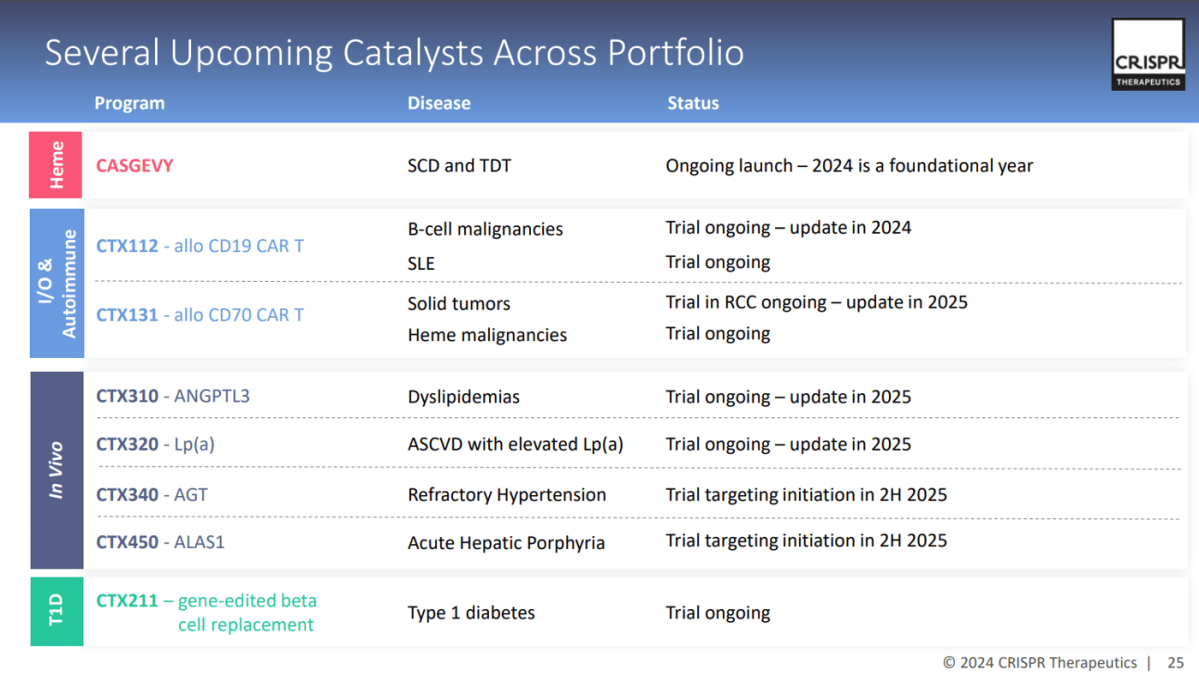

A part of CRISPR Therapeutics’ attraction as an funding is its first-mover benefit, which leverages a number of patented processes to CRISPR diagnostic and therapeutic functions. Casgevy approval, co-developed with Vertex Prescription drugshas validated its expertise to maneuver ahead with a broader pipeline of drug candidates.

A crucial a part of CRISPR is the requirement that therapies be constituted of stem cells harvested from particular person sufferers. CRISPR Therapeutics operates an industrial laboratory that gives strategic flexibility to scale operations. Its oncology, cardiology and diabetes applications have candidates in varied phases of scientific research and human trials.

For 2025, the corporate expects expanded steering for Casgevy, in addition to up to date efficacy knowledge for its pipeline of candidates, which may function potential catalysts for buyers to guage.

Picture supply: CRISPR Therapeutics.

There’s some optimism that CRISPR Therapeutics continues to be within the early phases of a major long-term alternative. The corporate’s steadiness sheet, with $1.9 billion in money, means CRISPR has the time and capital to take the required steps to turn into commercially viable.

Alternatively, the newest monetary developments depart a lot to be desired. Within the third quarter, CRISPR reported solely $602,000 in world income, not but materially capitalizing on the preliminary launch of Casgevy, marketed and distributed by Vertex.

The replace says just one affected person has acquired the industrial therapy, which prices $2.2 million. This large sum could also be justified by its lifesaving potential, but it surely additionally highlights the financial problem of widespread adoption. In line with Vertex, 40 sufferers have begun the complicated cell assortment course of that’s anticipated to end in accelerated collaboration income for CRISPR.

In line with Wall Road consensus estimates, out of projected income of $14 million this 12 months, CRISPR is predicted to generate $132 million in income for 2025 as Casgevy remedies achieve traction. But this isn’t sufficient to scale back what are anticipated to be important monetary losses over the approaching years. An estimated loss per share of $5.15 for 2024 is simply anticipated to slim to a lack of $5.02 subsequent 12 months.

This is not essentially an issue for a high-growth inventory, but it surely represents a steadiness sheet danger for buyers. If gross sales proceed to disappoint, the corporate’s inventory trades at a worth 31 occasions greater than subsequent 12 months’s gross sales because the ahead price-to-sales (P/S) ratio may very well be susceptible to an extended sell-off. essential.

CRISPR Therapeutics’ success will rely on its capacity to convey a number of new medicine to market to assist a extra viable enterprise mannequin.

On the similar time, the corporate will face rising competitors from different biotech gamers who’re utilizing comparable CRISPR strategies for drug growth. Firms like Intellia Therapeutic And Beam remedy are shifting ahead independently with their variations of gene-editing expertise that will show simpler for sure ailments.

It is usually unclear whether or not CRISPR is superior to various biotechnologies, akin to monoclonal antibodies or RNA-based therapies, which have generated latest advances. In the end, CRISPR Therapeutics exhibits nice promise, however there’s a lengthy street to turning into a worldwide participant. biotechnology chief.

Brief-term monetary weak point is purpose sufficient for me to remain away and keep away from CRISPR Therapeutics inventory for now. The corporate may very properly show to be a winner in the long term, however buyers ought to proceed with warning till there may be proof of some momentum in gross sales and earnings. I count on the inventory to stay risky.

Have you ever ever felt such as you missed the boat by shopping for the perfect performing shares? Then it would be best to hear this.

On uncommon events, our group of skilled analysts points a “Doubled” actions advice for companies that they imagine are on the breaking point. For those who’re nervous that you have already missed your likelihood to speculate, now could be the perfect time to purchase earlier than it is too late. And the numbers communicate for themselves:

Nvidia:For those who invested $1,000 after we doubled down in 2009,you’d have $348,112!*

Apple: For those who invested $1,000 after we doubled down in 2008, you’d have $46,992!*

Netflix: For those who invested $1,000 after we doubled down in 2004, you’d have $495,539!*

Proper now, we’re issuing “Double Down” alerts for 3 unbelievable corporations, and there is probably not one other likelihood like this anytime quickly.

And Victor has no place in any of the shares talked about. The Motley Idiot ranks and recommends Beam Therapeutics, CRISPR Therapeutics, and Intellia Therapeutics. The Motley Idiot has a disclosure policy.