Superior microdevices(NASDAQ:AMD) And Marvell Know-how(NASDAQ:MRVL) have seen contrasting fortunes within the inventory market in 2024, with one in every of these names making gorgeous beneficial properties whereas the opposite is within the purple.

Extra to the purpose, AMD’s inventory’s 13% decline this 12 months pales compared to Marvell’s inventory’s spectacular 76% rise. Each corporations are profiting from rising demand for chips to energy synthetic intelligence (AI). So, will Marvell stay the most effective AI Actions each in 2025 as properly? Or can AMD flip issues round within the new 12 months and surpass Marvell?

Let’s discover out.

AMD played the supporting role has Nvidia within the AI knowledge heart graphics processing unit (GPU) market. Regardless of this, the corporate’s knowledge heart enterprise has seen spectacular development.

Within the third quarter of 2024, for instance, AMD’s knowledge heart income elevated 122% year-over-year to a report $3.5 billion.

Administration says this spectacular development is pushed by sturdy demand for its knowledge heart GPUs and CPUs (central processing models). The corporate now expects to finish the 12 months with $5 billion in knowledge heart GPU income, which might be a big enchancment over the $400 million in income generated from the sale of those chips within the fourth quarter of 2023.

Moreover, the corporate has continued to extend its knowledge heart GPU forecast all year long, from $2 billion at first of the 12 months.

AMD can also be seeing success in different associated niches, akin to AI-enabled private computer systems (PCs). This explains why the corporate’s income from its buyer phase, which incorporates gross sales of processors utilized in desktops and laptops, elevated 29% 12 months over 12 months within the third quarter, to achieve $1.9 billion. These two segments collectively generated 80% of AMD’s income within the third quarter, and their sturdy development allowed the corporate to offset weak point in different areas akin to gaming and embedded chips.

The corporate’s general income elevated 18% from the corresponding quarter final 12 months to $6.8 billion, whereas adjusted revenue rose 31% to $0.92. per share. AMD’s steerage for the present quarter can also be sturdy. The corporate expects its year-over-year income development to speed up to 22% within the fourth quarter. Analysts predict that AMD will depart 2024 with a 13% enhance in income to $25.6 billion, in addition to a 25% enhance in earnings to $3.32 per share.

Subsequent 12 months, nonetheless, can be a lot stronger for AMD, according to consensus expectations. Its income is predicted to leap practically 27%, whereas income are anticipated to extend 54%.

It is easy to see why analysts anticipate AMD’s development to speed up considerably subsequent 12 months. First, AI-enabled PC shipments are anticipated to extend by 165% in 2025, in line with Gartner. This is able to be a serious enchancment over the 100% development anticipated for 2024.

AMD is well-positioned to capitalize on development on this market, in line with its third-quarter earnings name, through which it mentioned PC makers akin to HP and Lenovo “are on monitor to greater than triple the variety of platforms” Ryzen AI Professional varieties that they provide in 2024″. and we plan to have greater than 100 industrial Ryzen AI Professional platforms in [the] market subsequent 12 months.

In the meantime, AMD might additionally profit from improved AI GPU manufacturing by its foundry companion. TSMC in 2025. The Taiwan-based foundry big is predicted to double in measurement in 2025, and additionally it is anticipated to make use of its Arizona manufacturing plant to make AMD’s upcoming AI accelerators. There may be subsequently a very good likelihood that the corporate’s fortunes on the inventory market might enhance in 2025 because of AI.

Marvell Know-how is a key participant within the AI-driven application-specific built-in circuit (ASIC) market, an business that’s rising at a breakneck tempo. And demand for Marvell’s optical gear can also be rising considerably to allow sooner connections inside and between knowledge facilities. These catalysts are the rationale why its knowledge heart enterprise has seen unbelievable development in current occasions.

The chipmaker’s knowledge heart income elevated 98% year-over-year within the third quarter of fiscal 2025 (which ended Nov. 2) to $1.1 billion. The outstanding factor to notice right here is that the info heart phase generated 73% of Marvell’s income final quarter, in comparison with simply 39% final 12 months. The corporate’s knowledge heart development has been so good that it was sufficient to extend Marvell’s general income by 7% 12 months over 12 months, regardless of sturdy double-digit declines in its different 4 segments.

Administration says demand for its AI-specific chips is so sturdy that it’s on monitor to far exceed its full-year AI income forecast of $1.5 billion . Marvell is forecasting $2.5 billion within the subsequent fiscal 12 months.

Nevertheless, there’s a good likelihood that the chipmaker might additionally generate greater AI income subsequent 12 months because it has expanded its partnerships with main cloud computing suppliers akin to Amazon and attracted an extra buyer on board.

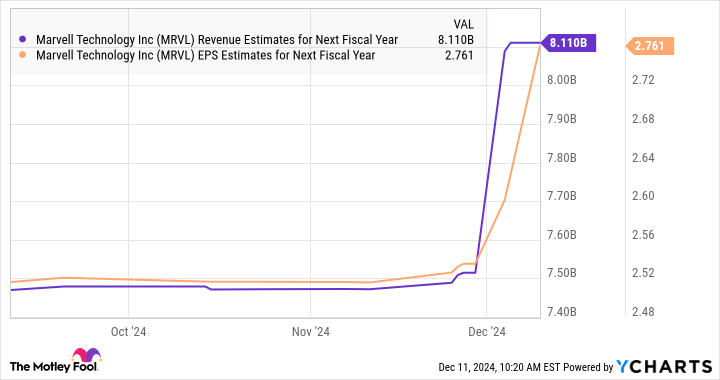

These catalysts are anticipated to be so highly effective that analysts predict a 41% enhance in income subsequent 12 months, to $8.1 billion, in addition to 77% development in internet revenue, to $2.76 per share. For comparability, the corporate’s income is predicted to develop simply 4% within the present fiscal 12 months, to $1.56 per share, together with a 3% enhance in earnings per share.

So there’s a good likelihood that Marvell inventory will preserve its red-hot rally in 2025 as properly.

We discovered that AMD and Marvell are anticipated to see spectacular development subsequent 12 months. Marvell is predicted to develop at a sooner fee than AMD, however there are a number of explanation why the latter might show to be a more sensible choice in AI.

First, AMD is cheaper. The inventory’s ahead gross sales and earnings multiples presently make it the most affordable inventory relative to Marvell.

Second, AMD is a extra diversified AI inventory. The corporate offers processors and GPUs not just for knowledge facilities but in addition for private computer systems, indicating that it might have a bigger addressable AI market than Marvell.

So traders in search of an AI inventory that may ship a mixture of worth and development may be tempted to purchase AMD over Marvell regardless of the previous’s poor inventory efficiency this 12 months.

Have you ever ever felt such as you missed the boat by shopping for the most effective performing shares? Then it would be best to hear this.

On uncommon events, our staff of skilled analysts points a “Doubled” actions advice for companies that they consider are on the snapping point. In case you’re anxious that you’ve got already missed your likelihood to speculate, now’s the most effective time to purchase earlier than it is too late. And the numbers communicate for themselves:

Nvidia:In case you invested $1,000 after we doubled down in 2009,you’ll have $348,112!*

Apple: In case you invested $1,000 after we doubled down in 2008, you’ll have $46,992!*

Netflix: In case you invested $1,000 after we doubled down in 2004, you’ll have $495,539!*

Proper now, we’re issuing “Double Down” alerts for 3 unbelievable corporations, and there will not be one other likelihood like this anytime quickly.

John Mackey, former CEO of Entire Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Hard Chauhan has no place in any of the shares talked about. The Motley Idiot holds positions and recommends Superior Micro Units, Amazon, Nvidia and Taiwan Semiconductor Manufacturing. The Motley Idiot recommends Gartner and Marvell Know-how. The Motley Idiot has a disclosure policy.