As traders most likely already know, Intel Corp (INTC) has change into the black sheep of the market. semiconductor household. Late within the transition from processors to GPUs, Intel misplaced its management within the sector to Nvidia (NVDA) and its long-time competitor Superior Micro Gadgets (AMD). This truth is abundantly clear when you think about that NVDA’s market capitalization is now roughly 40 instances that of Intel.

With Intel shares at all-time low, new management on the firm, in addition to sparks of buyout curiosity since Intel’s darkish days in August, many traders could also be optimistic a few turnaround of Intel’s valuation. On the present stage, I favor to attend however earn revenue via my dedication to purchasing INTC shares at a cheaper price. Formally, I supply a Maintain score on INTC.

Though the inventory has seen bigger market capitalization losses, Intel stock falls 26% on August 1, 2024was its greatest proportion decline in no less than the final decade. It was additionally preceded and adopted by buying and selling classes with losses better than 5%. The corporate has definitely upset traders on different events, however after publishing their results for the second quarter of 2024contrarian traders have been reluctant to purchase the dip. Intel’s enterprise relevance has been questioned by some analysts as margins have fallen sharply and the corporate has introduced plans for layoffs.

The company also suspended its dividend. Those that regarded nearer seen that Intel’s free cash flow (FCF) had turned negative in 2022 and that the corporate had internet debt of almost $30 billion whereas its outlook was declining. Intel had spent extra money than it had made for the reason that begin of 2023, and the second quarter 2024 outcomes primarily served as D-Day for the corporate’s current arc and technique.

Though traders have confronted appreciable challenges, INTC shareholders must be grateful that only a few massive dividend funds/ETFs will maintain the inventory this summer time. In any other case, the sale would have been a lot worse.

I nonetheless imagine Intel has worth. The corporate has tens of hundreds of patents and a long-standing repute for dependable chips. Though the corporate’s repute amongst traders could possibly be significantly broken, its repute amongst longtime PC prospects must be much less broken. This a part of the enterprise is anticipated to proceed to develop as the corporate works to regain its footing and advance its technological competitiveness within the AI period.

By way of graphics processing items, I think about the brand new administration workforce is setting modest objectives. Difficult Nvidia and AMD head-on would not appear practical, no less than not within the quick time period. Working to seek out an exploitable area of interest, such because the Arc B580, which has garnered favorable evaluations within the worth house, looks as if a great mid-term objective.

I feel the corporate may have many restructuring choices to contemplate, reminiscent of spinning off the Foundry and Merchandise companies, as has been rumored, and/or promoting half or all the firm. I feel it is a constructive signal that Intel hasn’t but rushed to do a take care of Qualcomm (QCOM) or different events. No firm desires to promote its enterprise on the level of most weak spot until completely needed.

One of many issues that considerations me is the co-CEO scenario that’s now established between Michelle Johnston Holthaus and David Zinsner. With so many vital choices to make, having two folks on the helm may result in some impasses.

INTC shares fell barely beneath the $20 stage in August/September, however rebounded above $26 after better-than-expected third-quarter leads to early November. It was a aid for traders to see margins rebound. Nevertheless, that shine wore off and the inventory returned to the $20 vary following the retirement of former CEO Pat Gelsinger.

I feel INTC inventory may see one other decline, probably as early as this month, attributable to tax-loss promoting. Moreover, some actively managed funds might want to take away INTC from their annual experiences till 2025.

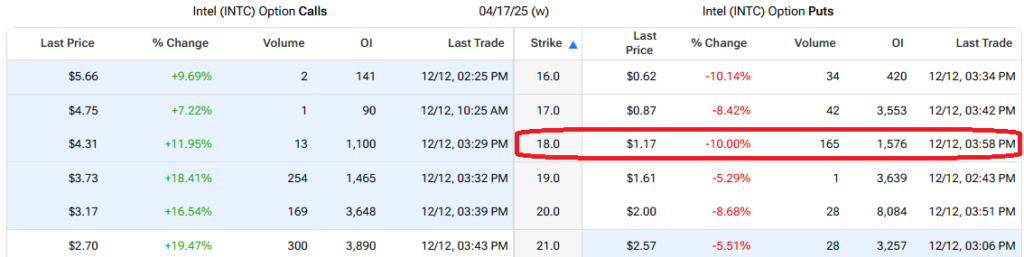

When Intel’s inventory crashed in August, I offered places at $17.50, and people lately expired, permitting me to pocket the premiums. I lately returned to this career and wrote some April 2025 $18 puts on INTC, which trade at a premium of around $1.17 (or $117 per contract). If Intel inventory fell beneath $18 and the places have been exercised towards me, I might have primarily gone lengthy INTC at $16.83. It’s positively a stage I’m snug at.

If INTC inventory stabilizes and doesn’t fall beneath $18 by April 17, 2025, I retain the choice premium of roughly $117 per contract.

Loads of Wall Avenue analysts stay hesitant in terms of Intel inventory. Of the 29 analysts who cowl INTC, there is just one purchase score in comparison with 22 maintain rankings and 6 promote rankings. THE INTC’s average price target is $24.43nonetheless, and represents an upside of over 20% from the present inventory value.

Whereas I feel Intel can flip round, I am not prepared to purchase frequent inventory but. There’s a affordable danger that shares will retest their early September 2024 low of $18.51 because the market weighs on the brand new administration workforce. Though the corporate is anticipated to submit a loss for the total 12 months 2024, analysts on common count on a restoration to succeed in EPS of $0.98 in 2025 (though estimates range broadly).

This may put INTC inventory at a ahead P/E of round 21x, which isn’t in any respect a discount value for an organization with the uncertainties it presents. I might reasonably commit to purchasing INTC at a 17x ahead P/E by promoting the April 2025 $18 places and incomes an revenue if the choice is just not known as towards me. Formally, I at present have a Maintain score on Intel inventory, similar to most shares on Wall Avenue.