Spotify know-how(NYSE:SPOT) has been one of many best-performing know-how shares on the earth since its IPO in 2018. The journey, nonetheless, has been fraught with pitfalls. The shares produced an annual whole return of 19%, in comparison with 14% for the S&P500 index, that means Spotify has overwhelmed the market over the previous seven years.

Nevertheless, in 2021 and 2022, Spotify’s story regarded dire. The music and audio streaming platform noticed an 80% decline, with buyers involved in regards to the lack of profitability of its enterprise mannequin. Since falling to $75 per share, the inventory has rebounded over the previous two years, marking a outstanding comeback for the corporate, whose market capitalization now stands at almost $100 billion.

And but, this inventory is never talked about in investor circles, even after this rise. Here is the normally ignored story of Spotify’s return to the inventory market and whether or not you can purchase shares right this moment.

The tip of 2022 was a darkish time for Spotify. This was the deepest level of the inventory’s decline. Wall Road was involved in regards to the firm’s deteriorating working margin, which fell to -7% within the third and fourth quarters of this 12 months.

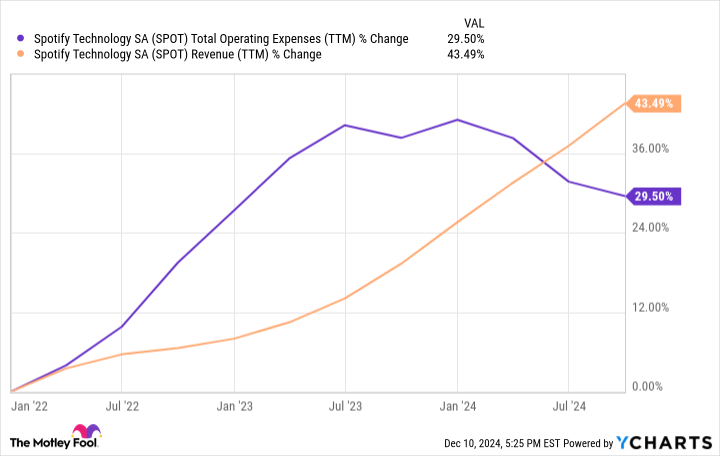

As a consequence of its formidable enlargement into podcasts, promoting and different new segments, Spotify’s working bills have grown sooner than income. Gross margins have additionally declined as a consequence of rising prices of podcast content material underneath costly licensing offers.

Within the two years since, Spotify’s margins have seen a miraculous turnaround. The explanation for this enchancment is straightforward: spending has been disciplined. Due to layoffs and fewer content material licensing offers, working bills have fallen from their peak, whereas gross margins hit a document 31.1% within the third quarter of this 12 months. On the identical time, income continued to develop and was up 19% year-over-year final quarter.

Better spending self-discipline led to a robust enchancment in working margin, which reached a optimistic 11.4% final quarter, surpassing administration’s earlier goal of reaching a revenue margin of 10%. % that it introduced at its 2022 investor day. That is implausible progress for an organization that many thought might by no means flip a revenue, which is why the inventory worth elevated by a a number of of 5 in lower than two years.

Income development has accelerated in current quarters, reaching 19% within the third quarter. Worth will increase for its premium subscriptions the world over are the primary motive for this development. The corporate has been in a position to implement important worth will increase in nations like america with little to no enhance in buyer churn, indicating that it’s underpricing its music service premium.

Worth will increase are good for shareholders, however Spotify cannot implement them yearly. Different sources of income development will come from buying new customers and new segments exterior of music.

Month-to-month energetic customers (MAUs) elevated 11% year-over-year final quarter to 640 million, with sturdy development coming from nations like Southeast Asia and India. With billions of individuals in these rising cell markets, there are many alternatives for development over the following few years.

Hopefully, these new clients will have interaction not solely with Spotify’s music service, but in addition with its different types of audio content material reminiscent of podcasts and audiobooks. The corporate lately launched audiobooks in choose markets to nice success, resulting in accelerated development within the class.

One other factor to focus on – and one that ought to result in additional revenue will increase – is gross margin enlargement. This metric reached 31.1% final quarter, up from 25% in 2022. Its promotional music market has helped garner higher unit economics from the music trade. If this gross margin enlargement continues over the following few years, the corporate could let extra earnings fall into its monetary outcomes.

The massive query for buyers is whether or not Spotify is a purchase after this monster run. As of this writing, the title has a market capitalization of $97.5 billion.

Income over the previous 12 months was $16.4 billion. If you happen to imagine in pricing energy, person development, and new audio segments, I feel it is believable that Spotify will develop income at an annual fee of 15% over the following 5 years. By way of higher scale and gross margin enlargement, I feel it is doubtless that its working margin will attain 15% over this five-year interval.

Making use of these estimates, revenues will attain $33 billion in 5 years and earnings can be slightly below $5 billion. Utilizing its present market cap of $97.5 billion, that represents a five-year price-to-operating earnings ratio of round 20.

There isn’t any motive to promote your Spotify shares at this worth, however including to your place or beginning a brand new buy right this moment appears unwise. If the corporate maintains this spectacular development, it can solely attain an earnings ratio near the long-term market common in 5 years. These are excessive expectations for the title. Keep away with Spotify (for now) after its monster run in 2024.

Have you ever ever felt such as you missed the boat by shopping for the very best performing shares? Then you’ll want to hear this.

On uncommon events, our group of professional analysts points a “Doubled” actions suggestion for companies that they imagine are on the snapping point. If you happen to’re frightened that you’ve got already missed your probability to speculate, now’s the very best time to purchase earlier than it is too late. And the numbers converse for themselves:

Nvidia:If you happen to invested $1,000 once we doubled down in 2009,you’ll have $348,112!*

Apple: If you happen to invested $1,000 once we doubled down in 2008, you’ll have $46,992!*

Netflix: If you happen to invested $1,000 once we doubled down in 2004, you’ll have $495,539!*

Proper now, we’re issuing “Double Down” alerts for 3 unimaginable firms, and there will not be one other probability like this anytime quickly.