The semiconductor business has skilled great progress over the previous few many years. Demand for chips could sluggish, particularly throughout financial recessions, however historical past reveals that extra superior gadgets and applied sciences require extra highly effective processors, creating an upward-sloping demand curve. Within the quick time period, artificial intelligence (AI) continues to be a key gross sales enabler for main chip suppliers.

IDC’s newest report predicts that the semiconductor market will develop 15% in 2025, pushed by demand for AI. This might present an awesome shopping for alternative for shares which have just lately fallen in worth.

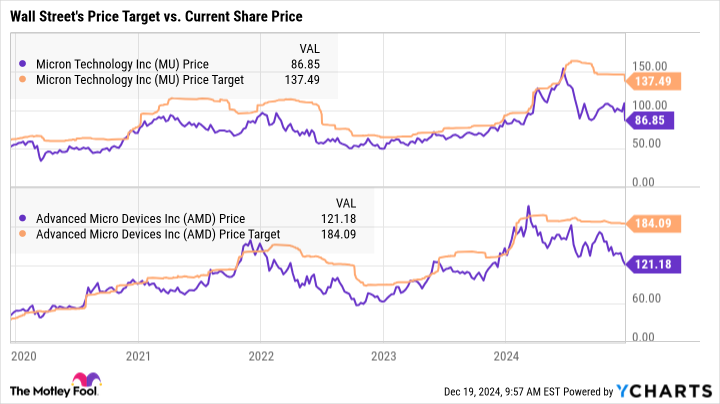

Two shares which are extremely valued on Wall Road are Superior microdevices(NASDAQ:AMD) And Micron know-how(NASDAQ:MU). These shares are buying and selling effectively above their latest highs however have reported robust income progress within the knowledge middle market.

The typical Wall Road price target is 55% increased than AMD’s inventory value, which stands at round $121, and 53% above Micron’s inventory value, which hovers round $87. Let’s take a more in-depth take a look at these corporations to see if it is sensible to guess your cash on Wall Road’s opinion.

Superior Micro Units inventory has generated distinctive returns lately. AMD is making many good points within the server market, which is reaching Intelat prices. Over the previous few years, its market share of central processing items (CPUs) utilized in servers has grown from single digits to 34%.

AMD can also be seeing robust demand for its graphics processing items (GPUs) within the knowledge middle market, and that is a possibility that would propel the inventory increased in 2025. Regardless of weak ends in the gaming markets and Within the business, AMD’s progress in knowledge facilities helped double its income progress within the third quarter in comparison with the identical quarter final 12 months. Analysts anticipate AMD to report year-over-year income progress of 13% for 2024, in line with Yahoo! Finance.

Subsequent 12 months, progress might speed up if demand in different segments picks up. For instance, AMD’s embedded chip income, together with gross sales to industrial markets, declined 25% 12 months over 12 months within the third quarter, however phase income elevated by 8% in comparison with the earlier quarter.

With AMD shares promoting 43% off their earlier highs and buying and selling at simply 23 instances the consensus estimate for subsequent 12 months’s earnings, Wall Road’s value goal could possibly be on the great path.

AMD expects the marketplace for AI accelerators, or GPUs, to develop greater than 60% yearly to succeed in $500 billion by 2028. It has an extended progress path forward and these processors superior gamers generate above-average revenue margins. This could permit income to develop quicker than revenues.

Analysts anticipate AMD to develop earnings at an annualized fee of 41%. For 2025, the road is looking for income to succeed in $5.13. If the inventory continues buying and selling at its present price-to-earnings a number of, the inventory value might rise with earnings and attain Wall Road’s value goal of $184.

After all, a sudden downturn within the chip business would dampen AMD’s momentum and restrict the inventory’s good points. However with the inventory value already buying and selling at a steep low cost to earlier highs, there’s a favorable risk-reward setup for AMD traders heading into 2025.

Micron Expertise is a number one supplier of reminiscence and storage merchandise to knowledge facilities, unique tools producers and client markets. The inventory has had a very good run since its 2022 low, with the share value up 71%. However shares are buying and selling effectively above their highs as demand for dynamic random entry reminiscence (DRAM) has weakened this 12 months.

The corporate simply launched its first quarter monetary outcomes, the place a dark outlook despatched the inventory decrease once more. Information middle gross sales elevated 400% year-over-year and 40% from the earlier quarter. Information middle gross sales now account for greater than half of Micron’s complete income.

Micron additionally mentioned its high-bandwidth reminiscence (HBM) shipments had been increased than anticipated, with HBM income greater than doubling from the earlier quarter.

These constructive demand developments had been offset by administration’s lackluster outlook for the fiscal second quarter. The income forecast was beneath Road estimates, however administration mentioned that was a short lived hurdle ensuing from stock adjustment by clients in consumer-related markets. The corporate expects this adjustment to be accomplished quickly.

Primarily based on its up to date outlook, Micron nonetheless expects to attain report income and constructive free money circulate in fiscal 2025 (which ends in August).

The inventory seems low cost at these decrease costs, however there’s a danger that it’s a worth entice. The issue is that Micron has an inconsistent working historical past. Regardless that revenues have grown steadily over the previous decade, the aggressive nature of the reminiscence market has induced giant swings in Micron’s earnings per share (EPS) and free money circulate.

The inventory is reasonable sufficient that if the corporate meets administration’s outlook for the complete 12 months, the inventory might return to its earlier highs. On the present value of $86, the inventory trades at 10 instances this 12 months’s estimated earnings and 6.6 instances fiscal 2026 estimates. These low valuation multiples are tempting.

Nonetheless, AMD gives the perfect risk-reward ratio and is the most secure guess to hit Wall Road’s 2025 value goal. Micron’s newest quarter reminds us that there are a lot of hard-to-predict variables which have a affect on the demand for its merchandise, which makes valuing the corporate a problem.

Have you ever ever felt such as you missed the boat by shopping for the perfect performing shares? Then it would be best to hear this.

On uncommon events, our staff of knowledgeable analysts points a “Doubled” actions advice for companies that they consider are on the breaking point. If you happen to’re anxious that you’ve got already missed your likelihood to speculate, now’s the perfect time to purchase earlier than it is too late. And the numbers communicate for themselves:

Nvidia:If you happen to invested $1,000 once we doubled down in 2009,you’ll have $349,279!*

Apple: If you happen to invested $1,000 once we doubled down in 2008, you’ll have $48,196!*

Netflix: If you happen to invested $1,000 once we doubled down in 2004, you’ll have $490,243!*

Proper now, we’re issuing “Double Down” alerts for 3 unbelievable corporations, and there will not be one other likelihood like this anytime quickly.

John Ballard holds positions in Superior Micro Units. The Motley Idiot ranks and recommends Superior Micro Units. The Mad Motley has a disclosure policy.