Gross sales within the semiconductor business are exploding due to secular trends synthetic intelligence (AI) and electrical autos (EV). The semiconductor market is predicted to succeed in greater than $600 billion in 2024, and attain $1 trillion by 2030, making investments in chipmakers a great way to capitalize on this progress.

Two semiconductor business leaders to contemplate are Wolf Velocity(NYSE: WOLF) And Nvidia(NASDAQ:NVDA). The previous has greater than 50% market share within the silicon carbide (SiC) wafer sector, whereas the latter made headlines as its inventory soared greater than 170% in 2024, throughout of the week ending December 13, due to its management in AI semiconductors.

Each provide progressive applied sciences that make them enticing investments. Let us take a look at Wolfspeed and Nvidia that can assist you consider which is the very best semiconductor inventory for the long run.

What makes Wolfspeed a worthwhile funding is its deal with silicon carbide (SiC). The corporate developed the primary business SiC wafers in 1991. They provide many benefits over the silicon extensively used at the moment within the semiconductor business, notably for electrical autos. Silicon carbide permits electrical autos to journey longer distances and cut back charging time.

Wolfspeed estimates its SiC gross sales will finally attain $3 billion in annual income as the electrical car market grows. For comparability, within the firm’s 2024 fiscal 12 months, which ended June 30, gross sales have been $807.2 million.

The potential of SiC seems promising, however the firm should first overcome a number of obstacles. It’s attempting to extend manufacturing at its SiC manufacturing crops, however the prices are excessive.

For instance, it generated income of $194.7 million in its fiscal first quarter ended September 29, however price of income got here in at $230.9 million. Due to this fact, gross profit of $77.4 million on the finish of fiscal 2024 become a lack of $36.2 million within the first quarter.

The nation can also be going through a cyclical slowdown, resulting in slowing gross sales. Its first-quarter income of $194.7 million was down from $197.4 million a 12 months earlier. Declining gross sales, lack of profitability and excessive manufacturing prices contributed to the resignation of Wolfspeed’s CEO in November.

With the rise of AI, Nvidia has turn into a semiconductor powerhouse. It’s now the world’s largest semiconductor firm by way of market capitalization.

CEO Jensen Huang anticipated the necessity for accelerated computing in 1999 and launched the graphics processing unit (GPU). Accelerated computing makes use of a devoted processor to deal with intense duties, similar to the information processing carried out by AI programs, somewhat than counting on a single processor to do every thing.

This pioneering work in GPUs has enabled the corporate to realize huge gross sales within the cloud computing sector, the place AI programs are hosted. Throughout its fiscal third quarter, ended October 27, Nvidia’s income hit a document $35.1 billion, a formidable 94% year-over-year enhance. This led to quarterly gross revenue of $26.2 billion, practically double the earlier 12 months’s $13.4 billion.

Nvidia’s AI merchandise are simply getting began. The corporate is rolling out its newest IT structure, referred to as Blackwell. The brand new platform “pushes the boundaries of scientific computing”, in line with administration.

This will probably be a key income supply. Huang mentioned present programs have been educated on human-generated information that existed earlier than AI. Immediately, AI is beginning to be taught from its personal synthetically produced content material.

This requires extra computing energy, which Blackwell gives. “So we’re seeing loads of demand coming from loads of totally different locations,” Huang mentioned, indicating that prospects proceed to want his firm’s merchandise for AI.

Between Wolfspeed and Nvidia, the latter’s robust gross sales, sturdy income, and regular demand appear to make it the apparent alternative between these two semiconductor giants. Nonetheless, inventory valuation is one other essential consideration.

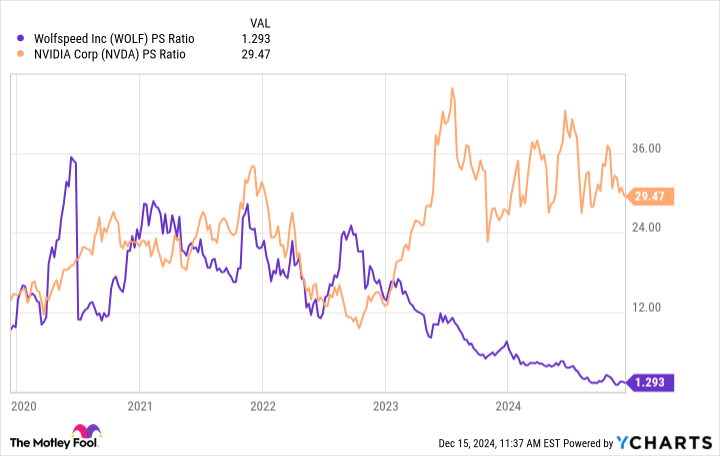

Evaluating Wolfspeed and Nvidia utilizing the price-to-sales (P/S) ratio, a metric measuring how a lot buyers are prepared to pay for every greenback of gross sales, is revealing.

Wolfspeed’s current struggles have brought about its inventory to fall greater than 80% this 12 months by December 13. In consequence, its P/S is the bottom in years, whereas Nvidia’s has carried out the other due to its AI success.

In consequence, Wolfspeed inventory seems to be the higher worth and will doubtlessly generate extra upside in the long run, if the corporate can get better from its present challenges. However because it faces plenty of short-term headwinds, solely buyers with a excessive danger tolerance ought to take into account shopping for the inventory.

For others, Nvidia’s success so far and the alternatives for continued gross sales progress with Blackwell make it the very best long-term funding within the semiconductor business.

Earlier than shopping for Nvidia inventory, take into account this:

THE Motley Idiot Inventory Advisor The analyst group has simply recognized what they suppose is the 10 best stocks for buyers to purchase now…and Nvidia wasn’t considered one of them. The ten shares chosen may produce monster returns within the years to come back.

Think about when Nvidia made this listing on April 15, 2005…in the event you had invested $1,000 on the time of our advice, you’d have $825,513!*

Fairness Advisor offers buyers with an easy-to-follow plan for fulfillment, together with portfolio constructing recommendation, common analyst updates, and two new inventory picks every month. THEFairness Advisorthe service has greater than quadrupled the return of the S&P 500 since 2002*.