THE S&P500 is on fireplace, constantly hitting report highs and posting robust performances over the previous two years. However relating to exceptional deeds, SoFi Applied sciences(NASDAQ:SOFI) has elevated by 261% for the reason that begin of 2023.

SoFi’s capability to develop its buyer base and improve income units it aside. After reporting its first quarterly web revenue a yr in the past, the fintech has maintained a worthwhile streak, recording a number of consecutive quarters of robust income.

SoFi is reaping the advantages of upper rates of interest, which have performed a central position in accelerating its buyer progress. With a number of alternatives for enlargement, the corporate is nicely positioned for continued success.

Nevertheless, with the inventory rising sharply this yr, potential buyers may be hesitant attributable to its excessive valuation. Let’s take a more in-depth take a look at SoFi to find out if it is a purchase, maintain, or promote on the present value.

Lately, SoFi has developed from a pupil mortgage refinancing firm to a monetary companies powerhouse. This significant change started throughout the pandemic when student loan forbearance has made its unique bread-and-butter enterprise a lot much less enticing.

SoFi has expanded considerably into private loans, assembly rising demand. However the actual sport changer got here in 2022 when SoFi acquired Golden Pacific Bancorp. This acquisition supplied SoFi with a basis for deposits and lending whereas offering it with the advantages of a conventional financial institution.

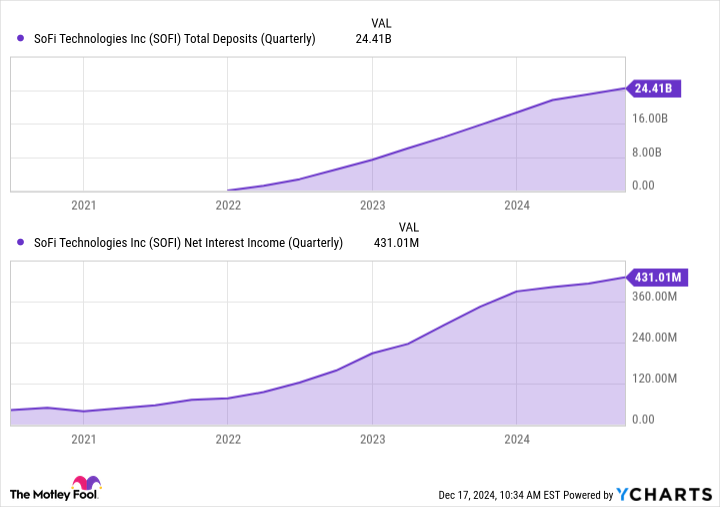

Outfitted with a banking constitution, SoFi has attracted numerous clients by providing annual returns of as much as 4.5% on their deposits. In consequence, SoFi buyer progress has exploded and deposits now stand at $24.4 billion.

The acquisition additionally means SoFi can retain extra of its loans, an enormous benefit within the current excessive rate of interest setting. The transfer helped the corporate’s web curiosity revenue climb to $431 million in its most up-to-date quarterly outcomes.

Moreover, the banking constitution allowed SoFi to develop its know-how infrastructure for non-bank entities. Fintech has made substantial investments in platforms like Galileo and Technisys, remodeling the fintech panorama.

By Galileo, SoFi supplies the important back-end companies that different fintech corporations depend on. On the identical time, Technisys helps assist a number of merchandise concurrently, operates on the cloud, and permits banks to course of and analyze knowledge in actual time. With this know-how stack, SoFi goals to be the Amazon Web Services (AWS) funds.

SoFi has grown rapidly and is performing extraordinarily nicely, which is why the inventory has risen a lot. Traders who’re bullish on this may occasionally discover the inventory value shopping for in the present day, even after its sharp rise.

Investor issues this yr have primarily targeted on SoFi’s lending enterprise. As famous above, the fintech has considerably expanded its private lending operations. Earlier this yr, CEO Anthony Noto just lately hinted at a extra cautious outlook amid continued macroeconomic uncertainty.

SoFi has a $16.7 billion private mortgage portfolio, making credit score high quality an necessary side of its enterprise. Within the third quarter, the corporate reported $147 million in private loans written off, leading to a web charge-off charge (NCO) of three.52%. Whereas this represents a slight improve from final yr’s NCO charge of three.44%, it exhibits an enchancment over the earlier quarter’s 3.84%.

Moreover, SoFi inventory has seen vital upside and is buying and selling at a excessive valuation. The inventory is presently valued at 163 occasions earnings and 4.3 occasions tangible e-book worth, an exorbitant determine in comparison with conventional banking shares. Even when we bear in mind the anticipated outcomes for subsequent yr, the inventory is valued at 68 occasions anticipated earnings.

As SoFi’s mortgage portfolio continues to point out resilience, the speedy rise in its inventory value may sign that it is time to take some chips off the desk.

SoFi has reported a number of worthwhile quarters and continues to develop its buyer base and income. Its execution has yielded spectacular outcomes for buyers.

Nevertheless, the inventory has seen vital upside and is buying and selling at a premium valuation. Whereas I am optimistic about SoFi’s long-term progress potential, this excessive valuation results in elevated volatility, each up and down.

After the current rally, buyers would possibly contemplate it a great time to cut back their place and take out a few of the income. That mentioned, I nonetheless like SoFi’s long-term outlook over the following decade, which is why I am giving it a Maintain ranking in the present day.

Have you ever ever felt such as you missed the boat by shopping for the perfect performing shares? Then it would be best to hear this.

On uncommon events, our crew of professional analysts points a “Doubled” actions advice for companies that they consider are on the snapping point. When you’re nervous that you have already missed your probability to take a position, now’s the perfect time to purchase earlier than it is too late. And the numbers converse for themselves:

Nvidia:When you invested $1,000 once we doubled down in 2009,you’d have $349,279!*

Apple: When you invested $1,000 once we doubled down in 2008, you’d have $48,196!*

Netflix: When you invested $1,000 once we doubled down in 2004, you’d have $490,243!*

Proper now, we’re issuing “Double Down” alerts for 3 unimaginable corporations, and there is probably not one other probability like this anytime quickly.

Courtney Carlsen has no place in any of the shares talked about. The Motley Idiot has no place in any of the securities talked about. The Mad Motley has a disclosure policy.