Actions of each Palantir Applied sciences(NASDAQ:PLTR) And Nvidia(NASDAQ:NVDA) have made beautiful beneficial properties this 12 months on rising demand for synthetic intelligence (AI) {hardware} and software program, though it is price noting that certainly one of these shares outperformed the opposite by a large margin.

Palantir inventory’s 345% beneficial properties (as of this writing) are considerably increased than Nvidia’s 188% bounce this 12 months. Nonetheless, does this make Palantir the very best AI Actions purchase each? Let’s discover out.

Nvidia could have made its title because the go-to chip provider for corporations trying to prepare AI fashions, however Palantir is the one serving to corporations and governments put these fashions into manufacturing. Extra importantly, the rising adoption of Palantir’s Synthetic Intelligence Platform (AIP), which permits companies to combine prolonged language fashions (LLM) and generative AI into their operations, has led to a powerful acceleration within the firm’s actions and revenues.

Its third-quarter 2024 income elevated 30% from the identical interval final 12 months to $726 million. For comparability, Palantir’s income grew at a a lot slower tempo of 17% in 2023. The corporate’s development accelerated because the 12 months progressed, with Palantir administration emphasizing throughout November earnings convention name that she “continues to see momentum pushed by AIP.” each when it comes to growth and acquisition of latest prospects.

It seems that Palantir’s buyer base grew 39% 12 months over 12 months. Deal sizes have additionally elevated, with the variety of offers price not less than $1 million rising 30% year-over-year final quarter to 104.

The corporate isn’t solely attracting new prospects for its AI software program platform; it additionally helps win extra enterprise from current prospects. That is evident in Palantir’s internet greenback retention charge of 118% within the third quarter, a metric that compares Palantir’s trailing 12-month income on the finish of 1 / 4 to the trailing 12-month income of the identical cohort of consumers throughout the 12 months. interval in the past. The corporate’s internet greenback retention throughout the identical quarter final 12 months was 107%, suggesting that current prospects have elevated their adoption of its platform.

Moreover, Palantir has a powerful income pipeline that also needs to enable it to take care of its spectacular development sooner or later. That is evident from the corporate’s remaining deal worth (RDV) price $4.5 billion, a metric that jumped 22% year-over-year within the earlier quarter . The spectacular development on this metric bodes nicely for Palantir, as RDV represents the overall remaining worth of the corporate’s contracts on the finish of a interval.

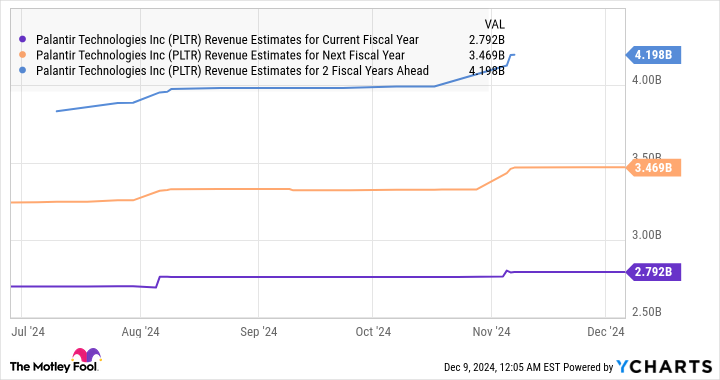

The dialogue above tells us why Palantir elevated its full-year steerage, projecting income of simply over $2.8 billion in 2024. That will symbolize a 25% improve. in comparison with 2023 income of $2.23 billion. Estimates for the following two years have additionally been elevated.

Graphic PLTR income estimates for the present fiscal 12 months

Because the chart above exhibits, Palantir’s income is predicted to develop by greater than 20% over the following two years. Nonetheless, do not be shocked to see the corporate see stronger development due to the large alternative within the AI software program platform market, an area that’s anticipated to develop at an annual charge of practically 41% till 2028.

Palantir due to this fact has the potential to stay one of many prime AI shares for a very long time.

Nvidia’s inventory returns this 12 months pale compared to Palantir’s, however buyers mustn’t neglect the crucial function the corporate performs within the proliferation of AI. The chipmaker reportedly controls greater than 85% of the AI information heart graphics processing unit (GPU) market, which explains why it has seen distinctive development quarter after quarter.

What’s price noting is that Nvidia’s dominance within the AI GPU market is so robust that its rivals are discovering it tough to make a dent within the firm’s enterprise. The corporate has reportedly offered out all of the capability of its new Blackwell graphics playing cards for subsequent 12 months, though the silver lining is that it’s taking steps to make sure that it can increase the supply.

Unsurprisingly, Nvidia is predicted to see one other 12 months of great development in fiscal 2026, following a stellar efficiency up to now this 12 months. Its income is predicted to develop 112% in fiscal 2025 to $129 billion, and the forecast for the following two years can be fairly robust.

Desk of NVDA’s income estimates for the present fiscal 12 months

Higher but, Nvidia stays a long-term development inventory, even after the exceptional beneficial properties over the previous two years. Catalysts comparable to rising demand for AI chips and enterprise software program, the transition to accelerated computing, the adoption of digital twins, and the rise in chip content material in automobiles are the explanation why Nvidia may very well be sitting on a complete addressable market price a whopping $1.7 trillion.

It is also price noting that Nvidia might grow to be a risk to Palantir within the enterprise AI software program house. CFO Colette Kress remarked throughout the firm’s newest earnings convention name:

We count on full-year Nvidia AI Enterprise income to extend by greater than 2x in comparison with final 12 months, and our pipeline continues to develop.

As such, Nvidia appears to be like like a extra well-rounded AI inventory than Palantir. Nonetheless, that is not the one purpose why he appears to be the higher AI selection of the 2.

We have already seen that Nvidia is rising at a quicker charge than Palantir. Extra importantly, Nvidia is predicted to develop at a quicker charge than Palantir over the following 12 months, regardless of being a a lot bigger firm. All of this makes shopping for Nvidia inventory over Palantir a no brainer, particularly after wanting on the following chart.

Nvidia is considerably cheaper than Palantir regardless of superior development. In actual fact, Palantir’s valuation is so wealthy that the inventory’s 12-month median value goal of $38 signifies a 50% draw back from present ranges. Nvidia, however, has a 12-month median value goal of $175, which might symbolize a 23% improve from its present stage.

Moreover, Nvidia seems to be the very best AI inventory to purchase, even in the long run, provided that it caters to a a lot bigger addressable market due to its rising presence in AI software program and dominance within the materials.

Have you ever ever felt such as you missed the boat by shopping for the very best performing shares? Then you’ll want to hear this.

On uncommon events, our crew of knowledgeable analysts points a “Doubled” actions suggestion for companies that they consider are on the snapping point. When you’re apprehensive that you’ve got already missed your likelihood to take a position, now’s the very best time to purchase earlier than it is too late. And the numbers converse for themselves:

Nvidia:When you invested $1,000 after we doubled down in 2009,you’ll have $350,239!*

Apple: When you invested $1,000 after we doubled down in 2008, you’ll have $46,923!*

Netflix: When you invested $1,000 after we doubled down in 2004, you’ll have $492,562!*

Proper now, we’re issuing “Double Down” alerts for 3 unimaginable corporations, and there might not be one other likelihood like this anytime quickly.

Hard Chauhan has no place in any of the shares talked about. The Motley Idiot ranks and recommends Nvidia and Palantir Applied sciences. The Mad Motley has a disclosure policy.