As an investor, keeping tabs on the investment habits of billionaire hedge fund managers can serve two purposes. First, it can spark new investment ideas by bringing attention to companies you may not have thought of. Second, it can help validate investment decisions already made.

Chase Coleman and his team at Tiger Global Management recently increased the hedge fund's stake in a popular way to invest in the artificial intelligence (AI) arms race: Semiconductor manufacturing in Taiwan (NYSE:TSM)commonly known as TSMC.

Missing the morning scoop?Breakfast News delivers it all in one fast, stupid, free daily newsletter. Register for free »

In the third quarter, Tiger Global Management increased its stake in the company by almost 20% and now owns 3.63 million shares (2.8% of its overall portfolio) valued at $671 million. The fact that the hedge fund is still buying suggests there may still be time for others to buy what is considered an expensive stock by some financial measures.

We are now in the fourth quarter, so the question is whether there is still time to buy TSMC. Let's take a closer look and see if an answer presents itself.

TSMC is the world's largest semiconductor chip maker, serving as a manufacturer for many of the world's largest technology companies and chip designers. Almost all companies in the high-tech industry use chips made by TSMC, including Apple, Qualcomm, advanced micro devices, And Nvidia. These companies don't have the facilities to produce the chips they design at scale, so they outsource this very complex work (some manufacturing processes involve several hundred precision steps) to TSMC.

This puts TSMC in a great position, as even competitors like Intel come there to manufacture the chips which are used in the composition of their products.

Because TSMC constantly pushes the boundaries of chip technology and repeatedly introduces new manufacturing innovations, it has established itself as a leading choice in the field. This can be seen in the growth of its AI-related production efforts. It appears that TSMC management was able to see the potential that AI offered as early as the second quarter of 2023, when TSMC management predicted that AI-related revenues would grow at a compound annual growth rate (CAGR) of 50% for the next five years and would ultimately represent a low-teens percentage of overall turnover. Management's forecasts may have underestimated the impact of AI on its revenue. During its recent third-quarter conference call, management noted that AI-related revenues are expected to triple for the year and are expected to represent around 15% of revenues in 2024.

Clearly, TSMC's growth is far from over.

TSMC is always pushing the boundaries of what is possible with chip manufacturing technology. Its 3 nanometer (nm) chips are among the best available today, and it is already working hard to bring its 2 nm chips into production. Management said production would increase in 2025 and reach full scale in 2026.

Demand for pre-orders is already strong, with management saying it exceeded demand for the previous two generations (3nm and 5nm chips). Indeed, these chips are developed to be much more efficient than previous generations. When a 2nm chip is configured to produce the same level of computing power as a 3nm chip, it uses 25-30% less power. Since energy costs are a huge expense for anyone running a huge data center, the cost savings from an efficiency upgrade that these chips could enable could quickly pay for themselves.

As a result, TSMC will likely see strong revenue growth in the coming years. This confirms management's long-term forecast of 15% to 20%. overall Revenue CAGR over the “next few years,” making it a stock that could easily beat the market.

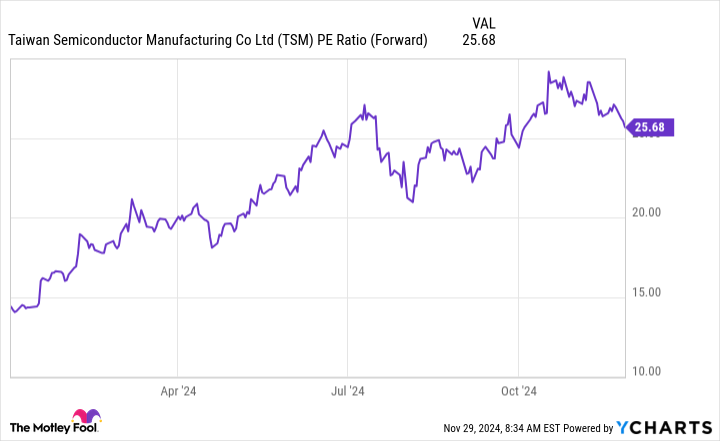

Despite estimates of strong growth over several years, TSMC stock still offers a reasonable valuation. TSMC stock trades at 26 times forward earningswhich is not a bad price to pay given that the broader market, as measured by S&P500trades at 23.5 times forward earnings.

Investors should feel pretty good about paying this slight premium for a company that's expected to grow revenue at a rate of 15-20% and has significant growth drivers on the horizon.

I already own TSMC stock, and seeing a billionaire add more shares after the stock has already had a good run in 2024 (up almost 87% so far in 2024) encourages me about the prospects future stock market performance of the company. Taiwan Semi is one of my best actions for 2025, and I think now is the perfect time to buy more.

Before buying Taiwan Semiconductor Manufacturing stock, consider this:

THE Motley Fool Stock Advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now…and Taiwan Semiconductor Manufacturing was not one of them. The 10 selected stocks could produce monster returns in the years to come.

Consider when Nvidia made this list on April 15, 2005…if you had invested $1,000 at the time of our recommendation, you would have $889,433!*

Equity Advisor provides investors with an easy-to-follow plan for success, including portfolio building advice, regular analyst updates, and two new stock picks each month. THEEquity Advisorthe service has more than quadrupled the return of the S&P 500 since 2002*.

Keithen Drury holds positions in semiconductor manufacturing in Taiwan. The Motley Fool holds positions and recommends Advanced Micro Devices, Apple, Intel, Nvidia, Qualcomm and Taiwan Semiconductor Manufacturing. The Motley Fool recommends the following options: Short February 2025 $27 calls on Intel. The Mad Motley has a disclosure policy.