Palantir Applied sciences(NASDAQ:PLTR) The inventory has seen a dizzying rise out there in 2024, posting exceptional positive factors of 370% as of this writing. The fast adoption of synthetic intelligence (AI) software program options by organizations and governments has performed a central function on this super evolution.

So if somebody bought simply $100 price of Palantir inventory on the finish of 2023, their funding would now be price $470. Nonetheless, in case you are a kind of who missed buy Palantir earlier than its surge begins in 2024 and are skeptical about investing within the inventory now as a result of its excessive valuation, there may be an fascinating different to think about within the type of Semiconductor manufacturing in Taiwan(NYSE:TSM).

Popularly referred to as TSMC, shares of this Taiwan-based foundry big have almost doubled in 2024. The excellent news is that this semiconductor big can nonetheless be bought at an affordable valuation, and buyers could wish to -be doing it instantly, because the essential function it performs within the chip trade might additionally trigger it to skyrocket in 2025.

Let’s check out why TSMC is without doubt one of the finest AI shares you should buy and maintain proper now.

The proliferation of AI is driving excessive demand for chips deployed in information facilities for coaching and inference, which has confirmed to be a boon for TSMC. Fabless chipmakers, reminiscent of Nvidia, Superior microdevices, Broadcom (NASDAQ:AVGO)And Marvell Expertisewhich design graphics processing items (GPUs) and application-specific built-in circuits (ASICs) to be used in AI information facilities, use TSMC manufacturing vegetation to make their chips.

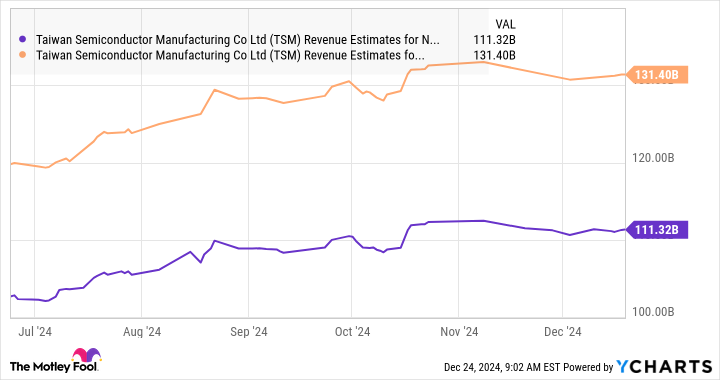

This is the reason the Taiwan-based firm has seen a giant enhance in income up to now in 2024. Within the first 11 months of the 12 months, TSMC’s income grew 32% year-over-year earlier. This can be a marked enchancment from TSMC’s 9% income decline to $69.3 billion in 2023. TSMC administration expects to see income development of 30%. for 2024 in US greenback phrases, which might deliver its income to $90 billion for the 12 months.

The optimistic factor is that consensus estimates additionally undertaking wholesome income development for the corporate for the following two years.

Nonetheless, latest feedback from main AI chip makers point out that TSMC could very nicely exceed market expectations sooner or later. Broadcom, for instance, generated $12.2 billion in income from AI chip gross sales in fiscal 2024, up 220% from the earlier 12 months. The corporate estimates that its addressable market in customized AI processors and networking chips may very well be between $60 billion and $90 billion by fiscal 2027.

That is greater than some analysts anticipated. Earlier this 12 months, Morgan Stanley valued Broadcom’s income alternative in customized AI chips at $20 billion to $30 billion, stating that this market is able to rising at a 20% compound annual development price. Based mostly on this development price, the customized AI chip market would have reached $51 billion in three years, on the excessive finish of the forecast vary.

So the newest feedback from Broadcom administration recommend the chance may very well be a lot greater. Extra importantly, Broadcom is working with TSMC and utilizing the latter’s superior chip packaging functionality to push the boundaries of the customized AI chip market to ship extra highly effective processors able to delivering higher efficiency.

Then again, TSMC will possible proceed to profit from robust demand for GPUs deployed in information facilities. AMD administration reported in October 2024 earnings conference call that the AI accelerator market measurement might develop at an annual price of 60% and attain $500 billion in 2028. Nvidia, however, sees a $1 trillion income alternative within the AI accelerator market. information via the shift from the overall AI accelerator market. from centered computing to GPU-powered accelerated computing.

Not surprisingly, TSMC is working to extend its capability so it may possibly produce extra chips to fulfill these clients’ demand for AI chips. In line with Taiwanese monetary newspaper Industrial Instances (by way of TrendForce), TSMC is predicted to double its superior chip packaging capability to 70,000 wafers per 30 days in 2025, adopted by an extra enhance to 90,000 wafers per 30 days in 2026.

The capability enchancment is predicted to allow TSMC to satisfy extra orders from clients that produce AI chips and finally keep strong top-line and bottom-line development.

Palantir’s inventory surge has made it fairly costly. Particularly, Palantir has a price-to-earnings ratio of 411, in addition to a ahead earnings a number of of 172. TSMC is less expensive on each of those fronts. Its present earnings a number of stands at 33, whereas the ahead earnings a number of stands at 23.

The fascinating factor to notice right here is that TSMC’s earnings are anticipated to develop at a sooner price, 27% to $8.93 per share in 2025, in comparison with Palantir’s forecast web development, 25% to 0.47 $ per share. So, TSMC is the considerably cheaper AI inventory to purchase proper now in comparison with Palantir, and shopping for it looks as if a no brainer on condition that the previous is predicted to see sooner earnings development.

Moreover, TSMC’s dominant place within the foundry market, the place it enjoys a strong 64% share, nicely forward of second-place foundry Samsung’s 12%, means it’s nicely positioned to profit from of the secular development of AI chips. All of this makes TSMC one of many high shares to purchase, and buyers who missed Palantir’s phenomenal rise can contemplate shopping for the Taiwanese foundry big earlier than it soars greater after spectacular positive factors in 2024.

Earlier than shopping for Taiwan Semiconductor Manufacturing inventory, contemplate this:

THE Motley Idiot Inventory Advisor The analyst workforce has simply recognized what they assume is the 10 best stocks for buyers to purchase now…and Taiwan Semiconductor Manufacturing was not one in all them. The ten shares chosen might produce monster returns within the years to return.

Contemplate when Nvidia made this listing on April 15, 2005…for those who had invested $1,000 on the time of our suggestion, you’d have $859,342!*

Fairness Advisor supplies buyers with an easy-to-follow plan for fulfillment, together with portfolio constructing recommendation, common analyst updates, and two new inventory picks every month. THEFairness Advisorthe service has greater than quadrupled the return of the S&P 500 since 2002*.

Hard Chauhan has no place in any of the shares talked about. The Motley Idiot holds positions and recommends Superior Micro Gadgets, Nvidia, Palantir Applied sciences and Taiwan Semiconductor Manufacturing. The Motley Idiot recommends Broadcom and Marvell Expertise. The Motley Idiot has a disclosure policy.