There’s by no means a foul time to purchase inventory. Should you can entry good inventory at a reduction, then nice. Finally, you’ll get a higher internet return in your invested {dollars}.

With that backdrop, this is a better have a look at three nice shares to purchase whereas they’re on sale. Word that every is no less than a little bit distinctive from the opposite two. So it would not be unsuitable to go for all three at these low costs.

Just a little over a decade in the past, the thought of hiring people driving their very own automobiles to create a fleet of taxis appeared outrageous. Now, carpooling isn’t solely commonplace, however a pioneer within the sector Uber Applied sciences(NYSE:UBER) is continually worthwhile, and more and more so.

Other similar things are also on the way. Anticipated income development of 17% this yr is predicted to be adopted by 16% development subsequent yr, with earnings per share anticipated to enhance even sooner.

Nevertheless it’s nonetheless only the start. Straits Analysis predicts that the worldwide ride-sharing and taxi providers market is predicted to develop at an annualized fee of 11.3% by way of 2032. Uber is poised to seize no less than share of that development – right here and overseas – due to his domination. of the North American market and its rising variety of partnerships overseas. For instance, final week the corporate co-launched a robotaxi service with WeRide in Abu Dhabi. And in October, Uber introduced it could use Avride’s autonomous supply robots to energy its Uber Eats meals supply service. Though small in scale for now, growth plans are already in place, together with one that can ultimately permit passengers to be carried.

traders ought to put together for continued volatility. It is nonetheless comparatively younger technology enterprise, in spite of everything, producing considerably unpredictable outcomes. Uber Applied sciences can also be thought-about economically delicate. That is the primary motive why the inventory has fallen 24% since its October peak.

Nevertheless, take a step again and have a look at the larger image. Uber now has sufficient scale to persistently cowl its mounted and variable prices, one thing it wasn’t certain it could be capable to obtain just some years in the past. Furthermore, it’s nearly sure that development from right here will probably be accompanied by even stronger revenue development.

The analyst neighborhood appears to assume so anyway. Its consensus goal of $90.89 is 39% above the inventory’s latest value. The overwhelming majority of this crowd additionally considers Uber inventory to be a gorgeous purchase.

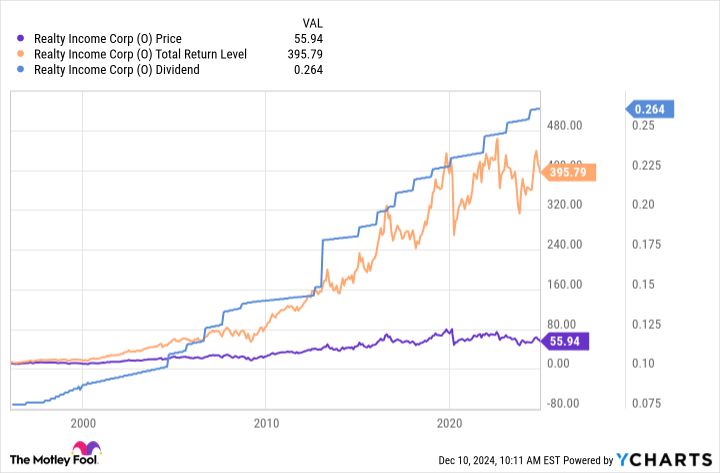

At first look Actual property revenue(NYSE:O) seems to be nothing greater than a dividend inventory (though it is an excellent one, with a ahead dividend yield of 5.6%). In case your funding purpose is above-average fast revenue, you may definitely do worse, particularly because the firm has elevated its dividend payout yearly for the previous 30 years.

Even when your purpose is internet development, there isn’t a must exclude this income-generating exercise.

It is not truly a inventory, for the report. Realty Revenue is a REIT, which is brief for actual property funding belief. These are firms that personal rent-generating properties like workplace buildings, resorts and condominium complexes; most of their internet earnings are returned to shareholders.

Even by REIT requirements, Realty Revenue is exclusive. You see, it focuses on retail areas and different consumer-facing companies.

This appears dangerous at first look. In any case, the bodily retail trade is perpetually defending itself towards the continued development of on-line purchasing. Coresight Analysis stories that as of early November, practically 6,500 shops in the USA have been closed because the finish of 2023, and greater than 40 retailers have declared chapter throughout that point.

However Realty Revenue primarily avoids these headwinds by leasing to the trade’s most resilient retailers. Its essential tenants embrace Greenback Tree, Walmart, FedExand 7-Eleven, to call a number of. With this in thoughts, on the finish of the third quarter, 98.7% of its industrial area was rented, thus sustaining its occupancy fee, the most effective within the sector, which solely fell to 97.9%, even at throughout a yr 2020 marked by a pandemic.

However internet capital appreciation? This is the issue: Whereas its superior, dependable dividend makes an excellent bullish case for income-minded traders, reinvesting that dividend in additional shares of the shares that pay them has truly produced near-growth outcomes for long-term house owners. The important thing has merely been to carry the place and reinvest these ever-increasing month-to-month (sure, month-to-month) dividends.

Lastly, add Coca-Cola(NYSE:KO) to your record of shares to purchase whereas they’re on sale when you’ve got an additional $1,000 to place to work for no less than a number of years.

Coca-Cola is, in fact, the world’s largest mushy drinks participant, though it represents way more than its namesake cola. Gold Peak tea, Minute Maid juice, Powerade sports activities drink, and Dasani water are just some of the opposite manufacturers which might be a part of the Coca-Cola household. This numerous portfolio of merchandise means the corporate at all times has one thing to supply shoppers, irrespective of how their preferences change.

That is to not say that Coca-Cola is resistant to all headwinds. Take the final quarter, for instance. Though its backside line of $11.95 billion and $0.77 per share (respectively) each beat expectations, the value will increase weren’t precisely effectively obtained. Complete quantity bought through the three-month interval fell 1%, inflicting income to say no by the identical quantity. This era of weak spot is the important thing motive why Coca-Cola inventory is down 15% from its September excessive.

As it is best to with Uber Applied sciences and Realty Revenue, take a step again and have a look at the larger image. Coca-Cola’s present headwinds aren’t one thing the corporate hasn’t confronted many instances up to now, popping out stronger every time. Whereas a 15% pullback might not be a large low cost, it might be the one low cost you will see in shares of this high-quality, confirmed beverage firm with a robust historical past of development at long run.

The Greatest: Whereas dividend revenue might not be your precedence proper now, this inventory’s 3.1% ahead yield is best than common and compelling even should you’re simply in search of a gradual move of money to purchase new development shares. This can be a quarterly dividend that has not solely been paid like clockwork for many years, however has additionally elevated in every of the final 62 years.

Earlier than shopping for Coca-Cola inventory, contemplate this:

THE Motley Idiot Inventory Advisor The analyst crew has simply recognized what they assume is the 10 best stocks for traders to purchase now… and Coca-Cola was not considered one of them. The ten chosen shares might produce monster returns within the years to return.

Contemplate when Nvidia made this record on April 15, 2005…should you had invested $1,000 on the time of our suggestion, you’d have $841,692!*

Fairness Advisor gives traders with an easy-to-follow plan for fulfillment, together with portfolio constructing recommendation, common analyst updates, and two new inventory picks every month. THEFairness Advisorthe service has greater than quadrupled the return of the S&P 500 since 2002*.

James Brumley holds positions at Coca-Cola. The Motley Idiot ranks and recommends FedEx, Realty Revenue, Uber Applied sciences and Walmart. The Motley Idiot has a disclosure policy.