As 2025 approaches, it is time to begin fascinated about which shares so as to add to your portfolio. Whereas I am a proponent of a well-diversified portfolio, I at present see a number of potential within the expertise house, particularly given the significance of synthetic intelligence (AI).

If you happen to’re in search of a listing of shares to purchase in 2025, here is a wide variety of 10 to select from.

If I had to purchase only one inventory from this checklist for 2025, I might select Semiconductor manufacturing in Taiwan (NYSE:TSM). Taiwan Semi is the world’s main contract chip producer and makes chips for nearly each firm that produces high-tech or AI-related merchandise.

Administration expects AI-related revenues to triple this 12 months, and there may be little likelihood this demand will gradual by 2025. Whereas Wall Road expects income progress of 25% in 2025, I might count on Taiwan Semi shares to excel subsequent 12 months.

Lastly, Taiwan Semi’s inventory just isn’t that costly, buying and selling at 22 instances 2025 earnings. Contemplating the significance of this firm, alongside its progress price and affordable value, it is among the most necessary shares to personal in 2025.

ASML(NASDAQ: ASML) is much like Taiwan Semi in that it is a crucial provider within the chip worth chain. ASML makes lithography machines that nobody else on the planet has the expertise to make, giving it a technological monopoly.

Nonetheless, this additionally poses issues as a result of its machines are extremely regulated and most can’t be offered in China. In consequence, administration minimize its income forecast for 2025, inflicting the inventory to fall, and it’s now down for the 12 months.

This near-term weak spot ought to be seen as a shopping for alternative, as ASML’s expertise is probably going unimaginable to copy or meet up with, so every little thing will likely be superb in the long run. Even with a downward information, Wall Road analysts nonetheless count on 15% progress subsequent 12 months, making ASML an fascinating inventory to purchase now.

Metaplatforms (NASDAQ:META) might be higher identified by its outdated identify, Fb. This social media big generates a ton of income and revenue from promoting advertisements, nevertheless it’s additionally concerned within the AI race.

Meta’s generative AI modelLlama, is the main open supply AI mannequin, making it a well-liked possibility for individuals who need visibility into what’s actually taking place behind the scenes. If Llama can change into the primary open supply AI mannequin, it’ll gather giant quantities of data quicker than different platforms that customers need to pay for, probably paving the way in which for a paid model.

Nonetheless, that type of success is a great distance off, and for now, traders ought to base their evaluation on the corporate’s promoting division, which is doing extremely effectively. Wall Road expects income progress of 21% for 2024 and 15% for 2025. With robust progress in hand, Meta ought to have a robust 2025, with AI probably one other tailwind that hasn’t not but contributed considerably to the enterprise.

Alphabet (NASDAQ:GOOG)(NASDAQ:GOOGL) is one other firm closely concerned within the AI race. Its Google Gemini mannequin is among the important choices, and it may be additional optimized by being deployed by Google Cloud, the corporate’s cloud computing wing.

Google Cloud grew 35% within the third quarter and is quickly enhancing its working margin. Though this phase represents solely a fraction of Alphabet’s whole income, it is among the most tasty facets of its enterprise and can enable it to attain above-market progress.

With shares lately buying and selling at a value 25 instances forecast earnings, Alphabet is attractively priced relative to lots of its massive tech friends.

AmazonIt’s (NASDAQ:AMZN) the funding thesis is much like that of Alphabet. Its core enterprise is flourishing (in Amazon’s case, an e-commerce empire), however the cloud computing division is the principle cause to purchase the inventory.

Amazon Internet Companies (AWS) accounted for 17% of income within the third quarter, however its working earnings represented 60% of the corporate’s whole. In consequence, AWS strongly drives the corporate’s earnings. With AWS posting wholesome 19% progress within the third quarter and no indicators of AI-related progress slowing, it is poised to push Amazon larger in 2025.

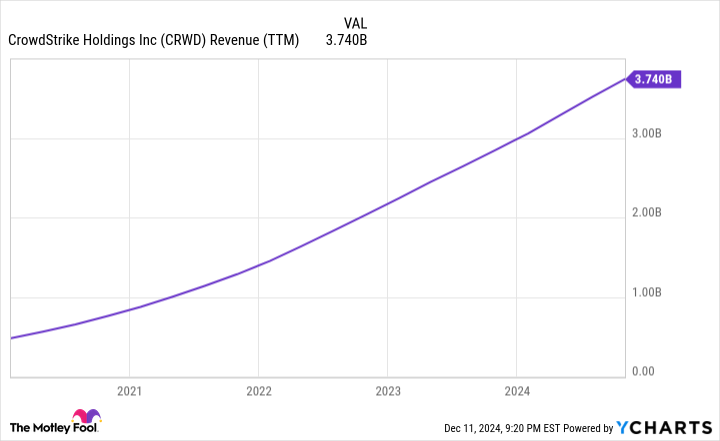

Crowd strike (NASDAQ:CRWD) could also be a little bit of a controversial title to incorporate on this checklist. CrowdStrike is a cybersecurity firm that gained visibility after a July 19 outage that crashed tens of millions of units. The consequences of the crash are nonetheless being sorted out, however that does not imply the corporate is not robust. CEO George Kurtz mentioned the corporate’s buyer portfolio had returned to pre-incident ranges, so the general impact was not too extreme.

In its most up-to-date quarter (which covers a full quarter after the incident), annual recurring income (ARR) grew 27% year-over-year to over $4 billion, which is on monitor to achieve its $10 billion ARR purpose.

CrowdStrike is a number one cybersecurity supplier; even a small stumble wasn’t sufficient to derail the enterprise. Though the inventory is a bit expensive, I believe it is value it given the expansion it is producing.

dLocal(NASDAQ:DLO) is a much more obscure firm than every other on this checklist. It gives a plug-in for anybody trying to course of funds in rising market international locations, opening entry to elements of the world that will not make monetary sense with out dLocal’s companies. Its shopper checklist contains giants like Amazon, Spotify expertiseAnd Shopifydemonstrating that its product occupies an necessary area of interest.

dLocal is within the midst of a metamorphosis with the arrival of recent CEO Pedro Arnt after a 12-year mandate at MercadoLibre. He ran an extremely profitable enterprise there and has the plan to reignite dLocal’s progress.

With the inventory buying and selling at simply 25 instances ahead earnings regardless of a revenue margin effectively beneath its earlier highs, this inventory is extremely worthwhile.

Talking of unbelievable values, Paypal (NASDAQ:PYPL) remains to be a fairly low-cost inventory. The fee processing big has had its ups and downs, however is at present rising, because of CEO Alex Chriss, who has been within the position for simply over a 12 months.

PayPal is not displaying probably the most spectacular progress, with income up 6% 12 months over 12 months within the third quarter and earnings per share (EPS) up about 6% as effectively. Nonetheless, the corporate is diligently working to develop its enterprise segments and is utilizing its money to repurchase shares at an affordable value.

Although the inventory is not as low-cost because it as soon as was, buying and selling at 19 instances ahead earnings, it is nonetheless a discount, particularly for the reason that inventory S&P500 trades at 22.5 instances ahead earnings. In consequence, I believe PayPal nonetheless has a number of upside potential, and it could possibly be the turnaround story of the 12 months in 2025.

Subsequent comes MercadoLibre. The Latin American e-commerce and fintech big frequently posts unbelievable outcomes 12 months after 12 months.

On a currency-neutral foundation, MercadoLibre’s income grew over 100% within the third quarter, demonstrating its spectacular platform. Though the corporate had a tough patch within the third quarter attributable to some unhealthy money owed in its credit score portfolio, this can be a quarterly difficulty that can come up occasionally.

Though the inventory just isn’t low-cost, at 56 instances ahead earnings, its robust and sustainable progress justifies this value. In consequence, I believe it is a phenomenal inventory to purchase in 2025.

Final however not least is Nvidia (NASDAQ:NVDA). Nvidia has dominated the market in every of the final two years, however I do not count on it to take action once more in 2025. Nonetheless, whereas the largest gamers in AI and cloud suppliers As computing continues to develop its computing energy, Nvidia’s graphics processing unit (GPU) gross sales stay poised to profit.

Moreover, Nvidia’s Blackwell structure, which gives important efficiency beneficial properties over the present Hopper structure, will attain full-scale manufacturing in 2025, growing Nvidia’s income.

Regardless of Nvidia’s large progress over the previous two years, Wall Road nonetheless expects its income to extend 51% subsequent 12 months. That is sufficient to justify Nvidia’s value for me, and I believe it is a strong purchase heading into 2025. don’t expect him to repeat 2023 or 2024 performances.

Earlier than shopping for Taiwan Semiconductor Manufacturing inventory, contemplate this:

THE Motley Idiot Inventory Advisor The analyst workforce has simply recognized what they suppose is the 10 best stocks for traders to purchase now…and Taiwan Semiconductor Manufacturing was not certainly one of them. The ten chosen shares might produce monster returns within the years to come back.

Think about when Nvidia made this checklist on April 15, 2005…for those who had invested $1,000 on the time of our suggestion, you’ll have $841,692!*

Fairness Advisor gives traders with an easy-to-follow plan for fulfillment, together with portfolio constructing recommendation, common analyst updates, and two new inventory picks every month. THEFairness Advisorthe service has greater than quadrupled the return of the S&P 500 since 2002*.

John Mackey, former CEO of Entire Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Suzanne Frey, an government at Alphabet, is a member of The Motley Idiot’s board of administrators. Randi Zuckerberg, former director of market growth and spokesperson for Fb and sister of Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Idiot’s board of administrators. Keithen Drury holds positions in ASML, Alphabet, Amazon, CrowdStrike, DLocal, MercadoLibre, Meta Platforms, PayPal, Shopify and Taiwan Semiconductor Manufacturing. The Motley Idiot holds positions and recommends ASML, Alphabet, Amazon, CrowdStrike, MercadoLibre, Meta Platforms, Nvidia, PayPal, Shopify, Spotify Know-how and Taiwan Semiconductor Manufacturing. The Motley Idiot recommends DLocal and recommends the next choices: lengthy January 2027 $42.50 calls on PayPal and brief December 2024 $70 calls on PayPal. The Motley Idiot has a disclosure policy.