Walgreens Boot Alliance(NASDAQ:WBA) is a well known title within the healthcare trade. Shoppers in the US and all over the world have been visiting their neighborhood pharmacies for generations.

Nevertheless, the corporate goes by means of tough occasions. Clumsy efforts to develop the corporate scuttled the stability sheet and triggered a 90% decline from the inventory’s peak.

Restoration efforts have begun. Administration is lowering stability sheet debt and there may be hope for an eventual return to earnings development. Buyers as we speak are taking a look at a lagging inventory with an 11% dividend yield that would maybe be an enormous winner. a millionaire maker if Walgreens will get again on its ft.

However is it seemingly? Or has the trade left Walgreens behind?

Walgreens Boots Alliance is among the largest pharmaceutical firms on the planet. Sarcastically, the prescribed drugs shoppers hunt down at a Walgreens retailer (Boots within the UK) are simply the carrot to get them within the door. Pharmacies function on razor-thin margins and make most of their income by promoting retail merchandise, meals and drinks whereas clients go to the shops. Walgreens generated almost $116 billion in income from its U.S. pharmacies in 2024, however solely made $2.1 billion in working revenue, a margin of 1.5%.

Competitors from new sources, akin to threats from mail order and e-commerce, has pushed conventional pharmacies to develop their enterprise fashions. For instance, CVS Well being acquired medical health insurance big Aetna in 2018. Walgreens selected to develop into care companies, a expensive and acquisition-heavy enterprise that ultimately inflated its costs and balance sheet.

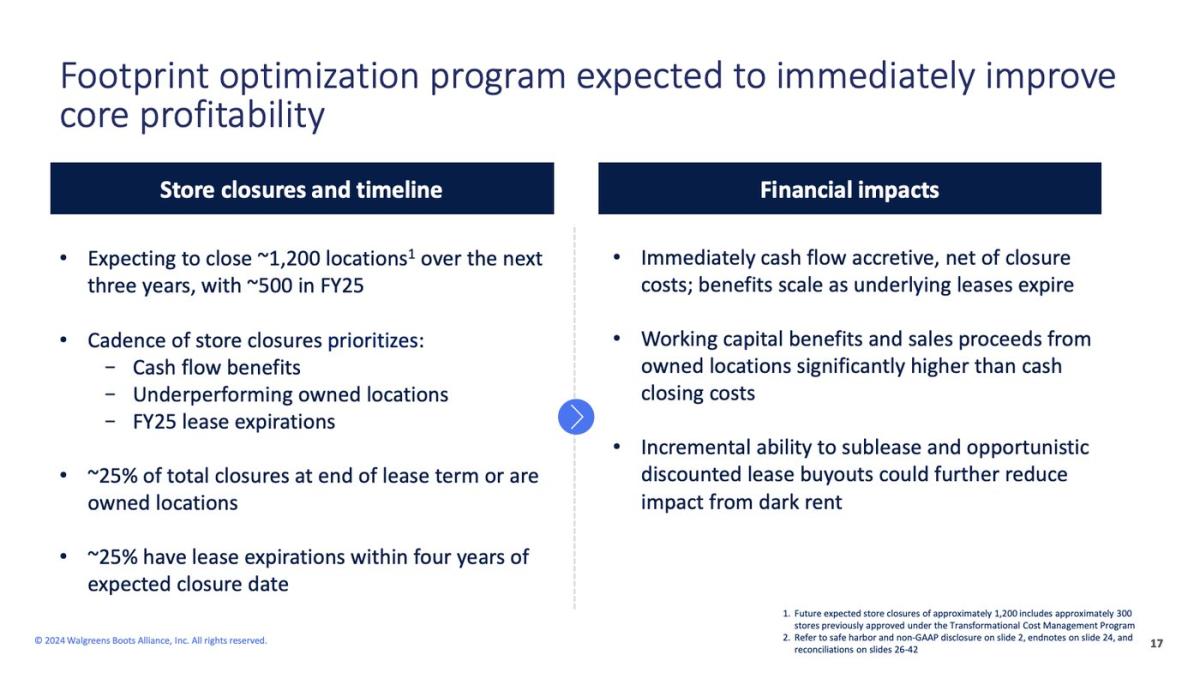

Immediately, the corporate is aggressively slicing fats. Administration deleverages the stability sheet and reduces prices by closing the least worthwhile shops:

Knowledge supply: Walgreens Boots Alliance.

The worst might quickly be over. Walgreens earned $2.88 per share in 2024 and initiatives 2025 earnings to say no to $1.40 on the low finish. Nevertheless, analysts estimate the corporate will develop earnings by a mean of 5% per 12 months over the subsequent three to 5 years, signaling a bottoming out and return to earnings development.

Assuming Walgreens will increase its income once more, the investment thesis is enticing at first look.

Walgreens trades at a ahead P/E ratio of round 6 and a PEG ratio of 1.1. In different phrases, the inventory’s valuation is enticing given the corporate’s anticipated earnings development. Buyers might hypothetically anticipate Walgreens inventory to generate funding returns akin to the corporate’s whole earnings development and dividend yield, or about 16% annualized.

The dividend is necessary right here since it might signify a substantial portion of the inventory’s hypothetical funding returns. Corporations set the quantity of the dividend, however it’s the inventory market that units the dividend yield. Keep in mind that a inventory’s dividend yield is a mathematical relationship between its dividend and the inventory worth. Extraordinarily excessive returns usually sign difficulties within the underlying companies. If the market had confidence within the dividend, the inventory would seemingly commerce at the next worth (and decrease yield).

Walgreens’ struggles are nicely documented, so it is honest to query the dividend. The present dividend per share of $1.00 represents as much as 70% of the corporate’s forecast earnings for 2025. Moreover, analysts requested administration in regards to the dividend in the course of the firm’s fourth-quarter earnings name in October, they usually haven’t dedicated to sustaining the present fee.

Walgreens may very well be an fascinating high-value inventory thought if the corporate manages to get again on monitor. However a inventory that brings in millionaires? Walgreens doesn’t seem to have this benefit.

The brick-and-mortar enterprise mannequin that Walgreens relies on is arguably outdated, with opponents in a position to ship on to shoppers. Your neighborhood pharmacy most likely will not disappear utterly anytime quickly, however there is a purpose Walgreens closes unprofitable shops. The dividend appears to be like set to be lower, particularly as Walgreens makes an attempt to show round its monetary scenario after ranking businesses downgraded its credit score to junk standing over the summer season. A dividend lower would seemingly go away traders with sluggish development and disappointing general returns.

As if that wasn’t sufficient, studies surfaced that Walgreens was contemplating promoting itself to a non-public fairness agency that might strip the corporate of its capital. A sale would seemingly require a premium to Walgreens’ present valuation. However given the corporate’s struggles, traders most likely should not anticipate something substantial that would generate an enormous acquire for shareholders.

In the end, it is most likely greatest to go away this well-known title within the trash fairly than in your pockets.

Have you ever ever felt such as you missed the boat by shopping for the most effective performing shares? Then it would be best to hear this.

On uncommon events, our group of skilled analysts points a “Doubled” actions suggestion for companies that they consider are on the breaking point. When you’re anxious that you have already missed your probability to speculate, now’s the most effective time to purchase earlier than it is too late. And the numbers converse for themselves:

Nvidia:When you invested $1,000 after we doubled down in 2009,you’ll have $348,112!*

Apple: When you invested $1,000 after we doubled down in 2008, you’ll have $46,992!*

Netflix: When you invested $1,000 after we doubled down in 2004, you’ll have $495,539!*

Proper now, we’re issuing “Double Down” alerts for 3 unbelievable firms, and there might not be one other probability like this anytime quickly.