Are you contemplating taking (or sustaining) a place in Sirius XM Holdings(NASDAQ:SERI)? If that’s the case, you aren’t alone.

Though its satellite tv for pc radio enterprise hasn’t precisely been scorching for some time, its 2019 acquisition of music streaming service Pandora, together with its new give attention to ad-supported radio, is attracting investor consideration for good motive. The inventory has carried out poorly recently, however some traders nonetheless see nice long-term potential within the new and improved Sirius.

Nonetheless, if you’re on the lookout for a extra confirmed work instrument, think about proudly owning a chunk of Costco wholesale(NASDAQ: COST) as an alternative. It made many extra millionaires than Sirius XM. There may be additionally a a lot better probability that this can proceed within the close to future.

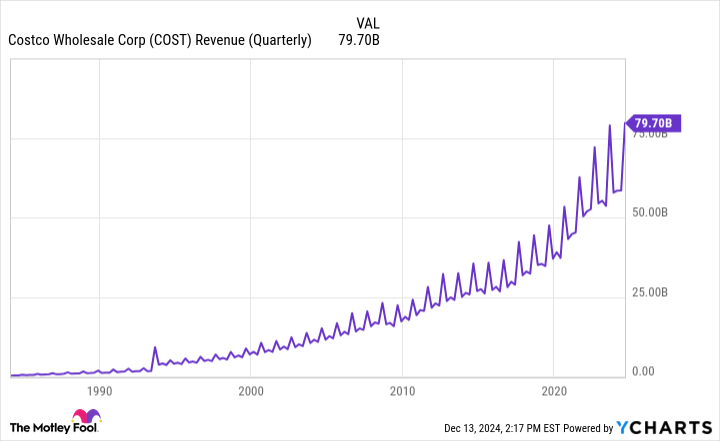

Costco is, in fact, the powerhouse of the membership sector retail business. As of late final month, practically 139 million cardholders have been paying $65 a 12 months (or $130 for extra advantages) for the proper to buy at its roughly 900 shops. The $440 billion firm has gross sales of round $250 billion a 12 months, of which greater than $7 billion is was web revenue.

This has been an actual engine of progress. Excluding a slight and short-lived spell in 2009 attributable to financial turmoil ensuing from the earlier 12 months’s subprime mortgage collapse, this retailer has reported gross sales progress each quarter since its IPO in scholarship in 1985.

Actually, constructing new shops has helped, however not as a lot as one may hope. Solely as soon as since 2019 has Costco reported a month-to-month decline in same-store gross sales. It was April 2020, when shutdowns as a result of COVID-19 pandemic made it inconceivable to proceed enterprise as traditional.

Information supply: Costco Corp. Chart by writer. Gross sales knowledge is in billions.

Like I stated, this firm is a heavy hitter. Actually, it’s now additionally a serious participant in a crowded and slowly altering market. Not solely does this oppose Walmart‘s Sam’s Membership, it additionally clearly competes with Amazon for individuals who spend cash. The 2 are powerful (to not point out larger) rivals.

Nonetheless, Costco nonetheless enjoys a handful of aggressive benefits that may proceed to make millionaires affected person traders. At first look, this looks as if a poor funding prospect. Whereas nobody denies that Costco is nice, promoting shopper items is not precisely a high-growth enterprise, regardless of how good you’re at it.

Nonetheless, do not overlook the long-term potential of this enterprise. The inventory’s 10,000% achieve over the past 40 years is not a really troublesome act to comply with – for a number of causes.

First, though the concept of paying an annual charge for the privilege of having the ability to store at a specific chain retailer might need appeared outrageous to many purchasers within the early days of the enterprise, individuals have turn out to be fairly snug with it. snug with subscription-based consumerism. From streaming companies to cell telephones to meal kits to software program to fitness center memberships, most individuals settle for that that is now a not-so-new norm.

This dynamic pairs properly with the opposite new dimension of contemporary retail. That is the empowerment supplied by the Web. By no means earlier than have individuals been higher outfitted to check costs after which crunch some numbers. Greater than 77 million households and companies have discovered that being a Costco member finally saves them cash, even with comparatively excessive annual charges and generally inconvenient bulk packaging.

This appears to work. CFRA Analysis experiences that membership shops like Costco are “successfully absorbing market share from supermarkets” as Hooks And by Albertson.

Immediately, this comparatively American phenomenon is spreading overseas. Though most Costco shops are positioned in the US (together with 108 in Canada), the corporate is now rising its worldwide arm as rapidly as its home operations. It opened three abroad shops final quarter, and plans so as to add 4 extra earlier than the tip of this monetary 12 months to deliver the quantity to 175.

In the meantime, the membership retailer plans to open 14 further shops in the US this 12 months, capitalizing on the still-mature buying preferences of home shoppers.

This may nonetheless solely scratch the floor of the multi-trillion greenback international shopper items market, which – if nothing else – continues to develop via inhabitants progress alone. The continued proliferation of telecommunications applied sciences and continued urbanization solely reinforce this tailwind. Costco will win extra enterprise if it provides itself the possibility to take action.

Is that this inventory poised for rapid, huge features? No. Even in good years, this retailer’s income progress is restricted to single digits. That is unlikely to alter within the foreseeable future.

The shares are additionally costly, buying and selling at 55 occasions this fiscal 12 months’s projected earnings per share, or $18.02. Analysts additionally appear involved about this valuation. Almost half charge Costco shares as a maintain quite than a purchase, whereas the inventory’s value is barely under analysts’ present consensus goal of round $1,011.

Costco could also be sluggish rising, however it’s a dependable producer in any atmosphere. The corporate has clearly mastered the artwork and science of membership-based warehouse buying. Income additionally develop sooner than revenues, with scale benefits more and more realized because the enterprise grows.

The very fact is, this can be a high quality enterprise that you must anticipate to pay a premium to take part in – even when a gaggle of analysts do not actually see it that manner in the intervening time. It isn’t simple to say the identical about Sirius XM proper now.

The trick? You simply should be prepared to stay with Costco for the lengthy haul to totally capitalize on its potential. It is a sluggish and regular commerce that wins the race, whereas Sirius XM leans extra towards an all-or-nothing, lightning-in-a-bottle perspective.

Earlier than shopping for shares in Costco Wholesale, think about this:

THE Motley Idiot Inventory Advisor The analyst workforce has simply recognized what they assume is the 10 best stocks for traders to purchase now…and Costco Wholesale was not one in every of them. The ten shares chosen may produce monster returns within the years to come back.

Think about when Nvidia made this checklist on April 15, 2005…when you had invested $1,000 on the time of our advice, you’ll have $822,755!*

Fairness Advisor gives traders with an easy-to-follow plan for fulfillment, together with portfolio constructing recommendation, common analyst updates, and two new inventory picks every month. THEFairness Advisorthe service has greater than quadrupled the return of the S&P 500 since 2002*.

John Mackey, former CEO of Entire Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. James Brumley has no place in any of the shares talked about. The Motley Idiot posts and recommends Amazon, Costco Wholesale, and Walmart. The Motley Idiot recommends Kroger. The Mad Motley has a disclosure policy.