Two of the most popular shares this 12 months are each darlings of the synthetic intelligence (AI) motion. Information evaluation software program developer Palantir Applied sciences(NASDAQ:PLTR) and cybersecurity specialist Crowd strike(NASDAQ:CRWD) have been within the highlight for a lot of 2024 – though for very totally different causes.

Whereas Palantir has finally proven Whereas it's a rising star in enterprise software program, CrowdStrike's status took a serious hit earlier this 12 months after a glitch in its platform brought on unprecedented outages for a lot of of its prospects.

Begin your mornings smarter! Get up with Breakfast Information in your mailbox each market day. Register for free »

Nonetheless, I stay optimistic about CrowdStrike's long-term narrative – a lot in order that I believe the corporate might be value greater than Palantir throughout the subsequent decade.

Under, I'll illustrate Palantir's speedy rise to the highest of the AI software program discipline and clarify how CrowdStrike may develop into probably the most beneficial firm in the long run.

As of this writing, Palantir inventory has gained 287% in 2024 and is the second finest performing inventory in the marketplace. S&P500.

The principle driver of Palantir's rise is the immense demand for its synthetic intelligence platform (AIP) software program. Till the discharge of AIP, Palantir was largely seen by skeptics as a consulting operation for the federal authorities with restricted software program capabilities. However over the previous 12 months, Palantir has turned that narrative on its head.

Over the previous 12 months, Palantir has elevated its buyer base by 39%. Much more spectacular, the corporate rapidly entered the personal sector, growing its variety of business prospects by greater than 50% within the 12 months ended September 30.

The plain profit of accelerating the variety of prospects is accelerated income. However what makes an funding in Palantir much more particular is the corporate's capacity to develop its margins and begin producing constructive free money circulation and web revenue alongside rising income.

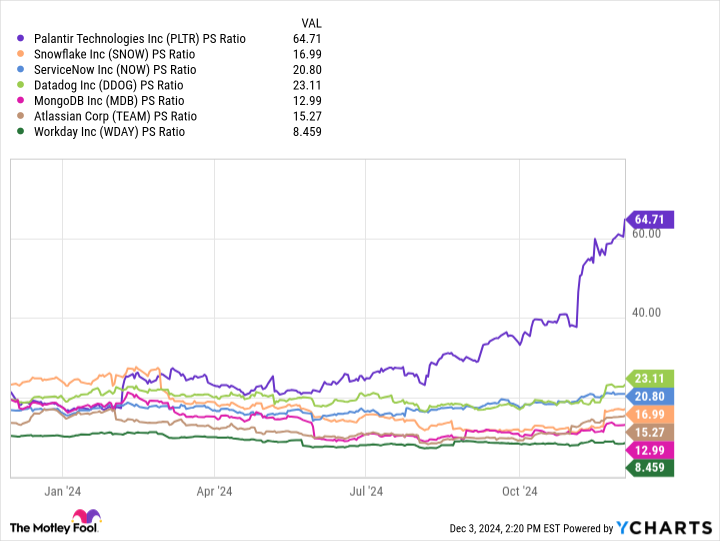

All of those elements make Palantir an apparent funding alternative… till you check out the chart under.

The plain outlier within the chart above is that Palantir's price-to-sales (P/S) ratio of 65 will not be solely the very best on this cohort, but it surely's additionally practically triple that of the peer firm the closest one. Whereas one may argue that Palantir deserves a premium a number of, the inventory has seen outsized valuation growth in an in any other case brief interval. Frankly, I believe it's this dynamic that’s inflicting some hedge funds to considerably scale back their publicity to Palantir and take income.

Picture supply: Getty Photos.

I'll make the apparent level clear up entrance: CrowdStrike is certainly not an inexpensive inventory. Even with the sell-off attributable to the safety outage over the summer season, the inventory nonetheless trades at a big premium to its friends.

Nonetheless, I see a number of key variations between an funding in CrowdStrike and an funding in Palantir.

As I explored beforehand, CrowdStrike was in uncommon firm a number of years in the past, through the peak of the COVID-19 pandemic. In actual fact, demand for CrowdStrike merchandise elevated through the COVID-19 recession. I see two causes for this. The plain purpose is that work-from-home protocols turned the norm through the peak days of the pandemic. That's why companies wanted to double down on cybersecurity protocols on enterprise units throughout this section of distant working.

Nonetheless, going additional, I’d argue that CrowdStrike is properly positioned in nearly any financial cycle as funding in cybersecurity turns into more and more non-negotiable.

In different phrases, whereas knowledge evaluation is essential, Palantir's worth proposition turns into more durable to justify in powerful instances when budgets are tight. In my view, the identical can’t be mentioned for cybersecurity.

The CrowdStrike safety outage incident occurred on July 19. A couple of month later, the corporate launched its outcomes for its second quarter of fiscal 2025 (ended July 31). For me, crucial quantity on this report was annual recurring income (ARR), which got here in at $3.9 billion.

Quick ahead to Q3, when CrowdStrike ended the quarter with simply over $4 billion in ARR.

Regardless of the reputational injury attributable to the outage, CrowdStrike nonetheless managed to extend its ARR over the previous two quarters. I believe it is a testomony to the superior high quality of the corporate's merchandise and the heavy reliance its prospects have on CrowdStrike's safety infrastructure.

Finally, I believe Palantir and CrowdStrike are costly shares. Nonetheless, Palantir's valuation is excessive and the inventory is overbought. As such, the corporate should show that it might obtain this premium valuation, which is not going to be a simple process given the depth of the enterprise software program panorama. Over time, it may develop into tougher to compete with current software program distributors, even when Palantir affords a superior product. Palantir's capacity to scale in the long run may come all the way down to pricing relative to competing platforms.

Then again, I consider companies will proceed to speculate extra in cybersecurity as fraud and ransomware threats enhance and develop into extra refined. Given CrowdStrike's confirmed capacity to develop throughout troublesome financial instances resembling recessions in addition to throughout business-specific troublesome instances (e.g. the outage), I consider the corporate is well-positioned to speed up its gross sales, enhance margins and enhance income over the approaching years.

For these causes, I believe CrowdStrike has a greater probability of seeing an elevated valuation from present ranges and will surpass that of Palantir if the software program developer exhibits indicators of extended development.

Have you ever ever felt such as you missed the boat by shopping for the most effective performing shares? Then it would be best to hear this.

On uncommon events, our staff of knowledgeable analysts points a “Doubled” actions suggestion for companies that they consider are on the breaking point. In case you're apprehensive that you just've already missed your probability to speculate, now’s the most effective time to purchase earlier than it's too late. And the numbers converse for themselves:

Nvidia:In case you invested $1,000 after we doubled down in 2009,you’ll have $369,349!*

Apple: In case you invested $1,000 after we doubled down in 2008, you’ll have $45,990!*

Netflix: In case you invested $1,000 after we doubled down in 2004, you’ll have $504,097!*

Proper now, we're issuing “Double Down” alerts for 3 unimaginable corporations, and there will not be one other probability like this anytime quickly.

Adam Spatacco holds positions at Palantir Applied sciences. The Motley Idiot holds positions and recommends Atlassian, CrowdStrike, Datadog, Fortinet, MongoDB, Okta, Palantir Applied sciences, ServiceNow, Snowflake, Workday and Zscaler. The Motley Idiot recommends Palo Alto Networks. The Mad Motley has a disclosure policy.