It would be an understatement to say that Palantir Technologies(NASDAQ:PLTR) The stock has been in good shape in the market in 2024, as shares of the software platform specialist have soared 290% so far this year as of this writing.

The last month alone has been great for Palantir investors as the stock has soared 62% since reporting its third-quarter results on November 4. Artificial Intelligence (AI) has been instrumental in this red-hot rally as businesses and governments have flocked to Palantir to help them integrate generative AI into their operations, helping the company accelerate growth and build a strong revenue pipeline .

Start your mornings smarter! Wake up with Breakfast News in your mailbox every market day. Register for free »

Wall Street, however, doesn't expect Palantir stock to maintain its momentum in 2025. Let's see why.

The 20 analysts who cover Palantir have a one-year price target of $38 for the stock. This suggests a 43% decline from current levels. Another thing to note is that 35% of analysts recommend selling Palantir stock. Half of them have a “hold” rating, while only 15% recommend buying.

Additionally, the high price target of $75 suggests that Palantir stock could only jump 12% from its current level over the next year. Valuation is one of the main reasons why analysts don't see much upside for Palantir stock. After all, Palantir now trades at 62 times its sales price. Its current price-to-earnings (P/E) ratio stands at 342. Although the forward earnings multiple of 137 points to an improvement in its bottom line, it remains very wealthy.

It is worth noting that these multiples are much higher than those of the AI pioneer. Nvidiaa company that has been grow at a much faster rate than Palantir. For example, Nvidia's revenue in its most recent quarter increased 94% year-over-year, to $35.1 billion. Its profit jumped 103% to $0.81 per share.

Palantir, on the other hand, reported a 30% increase in third-quarter revenue, to $726 million. The company's adjusted earnings increased 43% from last year to $0.10 per share. Of course, this is not an ideal comparison, because Nvidia is primarily a hardware company that is also successful in AI software, while Palantir is a purely specialized software provider.

However, the fact that Nvidia is growing at a much faster rate despite its larger size and trading at a price well below 32 times that of Palantir, makes Nvidia a much more logical AI stock to invest in this moment. Additionally, Palantir's valuation puts it at risk of a selloff if there are cracks in its growth, meaning it will need to continue to deliver stronger growth quarter after quarter to justify its rich multiples.

While there's no doubt that Palantir's valuation suggests the stock may have gotten ahead of itself, there are some things working in the company's favor that could be favorable for the stock next year.

First, Palantir's revenue growth rate has improved in each quarter of 2024. Its revenue grew 21% year-over-year in the first quarter, followed by a 27% increase. in the second trimester. We've already seen that its revenue jumped 30% last quarter, thanks to strong demand for the company's AI software platform.

The second reason why Palantir might be able to sustain its impressive rebound is its impressive growth in its customer base and deal size, which allows it to build a healthy long-term revenue pipeline. Specifically, Palantir's customer base grew 39% last quarter. The number of million-dollar contracts signed by the company increased from 80 to 104 last year.

As a result, the remaining transaction value (RDV) of Palantir's contracts increased 22% to $4.5 billion last quarter. Since this metric refers to the total remaining value of contracts the company was on at the end of the quarter, its impressive growth suggests that Palantir is able to continue growing revenue at a good pace over the long term.

The third reason why Palantir may still look attractive to growth investors is the strength of its unit economic structure. The company's non-GAAP operating margin in the third quarter was 38%, compared to 29% for the same period last year. Unit economics refers to the profit a company makes on each customer or product it sells after expenses are deducted.

The unit's favorable economics suggest that Palantir is now making more money from its customers, and that's not surprising. During the company's November earnings conference call, management gave several examples of customers expanding their contracts after signing up to use its solutions. This trend may continue in the future, as the market for AI software platforms is currently in its early stages of growth.

IDC predicts that spending on AI software platforms could increase from $27.9 billion in 2023 to $153 billion in 2028. As a result, adoption of Palantir's offerings is expected to improve further in the long term. term, and its strong unit economics should ideally enable it to maintain its impressive earnings growth.

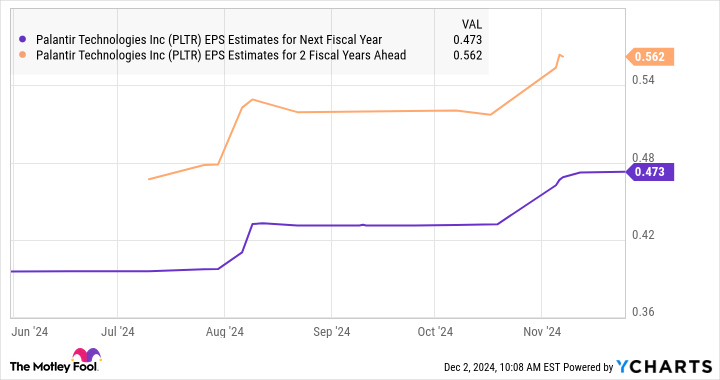

The above factors explain why analysts have increased their expectations for Palantir's earnings growth for 2025 and 2026.

If Palantir can continue to outperform analyst expectations over the next year and achieve higher levels of revenue and profit growth, there is a good chance that it will be able to justify its valuation and to go higher in 2025. Conservative investors would do the trick, however. It's worth considering other options if they're looking to capitalize on the AI boom, as Palantir's high valuation makes it prone to volatility.

Before buying Palantir Technologies stock, consider this:

THE Motley Fool Stock Advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now…and Palantir Technologies was not one of them. The 10 stocks selected could produce monster returns in the years to come.

Consider when Nvidia made this list on April 15, 2005…if you had invested $1,000 at the time of our recommendation, you would have $889,004!*

Equity Advisor provides investors with an easy-to-follow plan for success, including portfolio building advice, regular analyst updates, and two new stock picks each month. THEEquity Advisorthe service has more than quadrupled the return of the S&P 500 since 2002*.

Hard Chauhan has no position in any of the stocks mentioned. The Motley Fool ranks and recommends Nvidia and Palantir Technologies. The Mad Motley has a disclosure policy.