SoFi Applied sciences‘ (NASDAQ:SOFI) the corporate has been rising steadily since its IPO in 2020. The identical cannot be mentioned for its inventory value. SoFi inventory has lagged the market since its debut, posting a complete return of 46% in comparison with 77% for S&P500 index holders. The inventory value has underperformed index funds for years, doubtless irritating traders.

The underlying enterprise grew a lot quicker. Income grew 263% in whole, making it one of many fastest-growing firms on the general public markets since its shares started buying and selling. Does this fast progress and inventory value underperformance make SoFi a purchase at present? The place will or not it’s in 5 years? It is time to take a more in-depth take a look at this monetary expertise (fintech) disruptor and see if it has a spot in your portfolio at present.

SoFi began in 2011 as a pupil mortgage market at Stanford, and finally started its enterprise in pupil mortgage refinancing. Right this moment, it has turn out to be an all-in-one cellular app in your private monetary wants.

Banking providers, investments, lending merchandise, even cryptocurrencies and personal market investments: you’ll find all of it on the SoFi app. This speak, together with SoFi’s aggressive advertising campaigns, has led to regular progress in customers throughout SoFi’s numerous merchandise. It had 9.4 million members within the third quarter, in comparison with simply 1 million within the first quarter of 2020.

In 5 years, I anticipate this progress system may have led to much more utilization and model consciousness. In the USA, SoFi can goal greater than 100 million households. This does not simply apply to on-line banking, however nearly any monetary service a shopper may need. SoFi’s progress price will undoubtedly gradual (it is a aggressive trade, in spite of everything), however SoFi clearly has a price proposition that resonates with customers. I would not be shocked if the whole variety of clients reaches 20 million in 5 years.

A couple of years in the past, nearly all of SoFi’s enterprise was in lending. This included pupil loans but in addition private loans and residential loans. The corporate nonetheless operates on this area at present, and traders ought to anticipate its mortgage portfolio to develop as SoFi continues to amass buyer deposits. Complete excellent loans have been $25 billion within the third quarter, in comparison with $23 billion within the second quarter of 2024.

Buyers have been involved about SoFi’s mortgage efficiency as an unproven and fast-growing lender. SoFi has allayed these considerations, exhibiting credit score efficiency knowledge that signifies its present loans are performing higher (that means fewer debtors are defaulting) than in 2017. That is excellent news and it is in all probability the explanation the inventory soared after final quarter’s earnings.

Nonetheless, over the subsequent 5 years, I predict that SoFi’s enterprise will turn out to be more and more reluctant to lend. This has already occurred lately. The corporate’s monetary providers (bank card income, funding brokerage income) and expertise platform income now symbolize 49% of general income, up from 24% within the first quarter of 2021. Each segments are experiencing fast progress and will help SoFi diversify its operations, making it much less more likely to face a credit score downturn.

Its expertise platform, known as Galileo, helps third-party monetary establishments carry out operations akin to digital account setup and direct deposits. That is high-margin income that reached $100 million final quarter, rising 14% year-over-year. Galileo and the expertise providers enterprise are anticipated to contribute to SoFi’s earnings progress over the subsequent 5 years.

Estimating SoFi’s monetary efficiency is tough given its completely different enterprise segments. The mortgage transaction must be valued like a financial institution, which might use e book worth and web curiosity earnings as the first valuation metrics. Different segments akin to monetary providers and expertise platform could be significantly better valued when it comes to turnover and contribution margin.

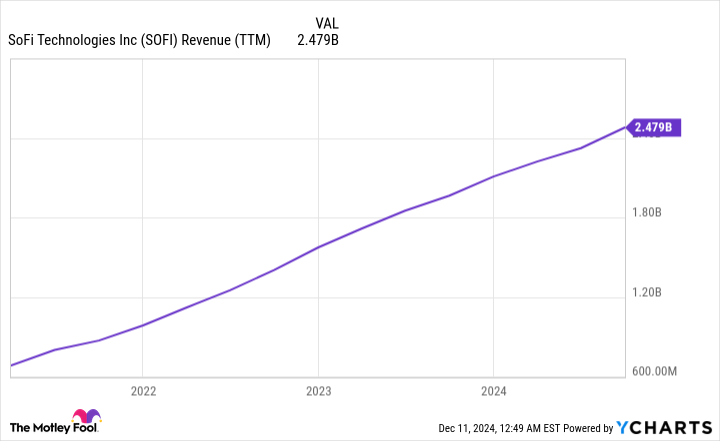

Let’s attempt to simplify issues to see if SoFi inventory is a purchase at at present’s costs. Over the previous 12 months, income was $2.5 billion. As a consequence of its enterprise momentum in person acquisition and buyer deposits, I imagine SoFi’s income can double over the subsequent 5 years to $5 billion. The corporate is not incomes a lot web revenue at present, however it’s doubtless that web revenue margins will attain 10% (if no more) as soon as the corporate matures over the subsequent 5 years.

This is able to convey SoFi’s annual web revenue to $500 million in 5 years. In comparison with its present market capitalization of $17.7 billion, this could symbolize a price-to-earnings ratio (P/E) of 28 in 5 years, which is increased than the present P/E of the S&P 500, now under 26. After all, SoFi’s revenues may greater than double in 5 years and the online revenue margin could possibly be over 10%. , however below On this state of affairs, the inventory would nonetheless be buying and selling at a number of instances increased earnings 5 years from now. From my perspective, the inventory appears a bit overvalued at present ranges. I would not anticipate shares to be a lot increased in 5 years.

Earlier than shopping for SoFi Applied sciences inventory, take into account this:

THE Motley Idiot Inventory Advisor The analyst workforce has simply recognized what they assume is the 10 best stocks for traders to purchase now…and SoFi Applied sciences was not one in every of them. The ten shares chosen may produce monster returns within the years to come back.

Take into account when Nvidia made this record on April 15, 2005…in case you had invested $1,000 on the time of our suggestion, you’ll have $822,755!*

Fairness Advisor offers traders with an easy-to-follow plan for fulfillment, together with portfolio constructing recommendation, common analyst updates, and two new inventory picks every month. THEFairness Advisorthe service has greater than quadrupled the return of the S&P 500 since 2002*.

Brett Schaefer has no place in any of the shares talked about. The Motley Idiot has no place in any of the securities talked about. The Mad Motley has a disclosure policy.